Technical Committee on Mobile Banking - Report

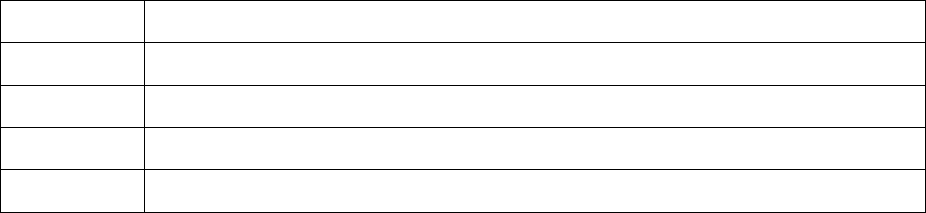

Members

Mr. Anand Rao

(Member)

Ir. Anthony Thomas

(Member)

ilip

Asbe

er)

Mr. C N Ra

(Member)

Mr.Pravir

Vohra

Mr.

Vijay

Chugh

(Member) (Member Secretary)

—-?\

Mr. B Sambamurthy

(Chairman)

Contents

Chapter No Particulars Page

Number

Letter of Transmittal

List of Abbreviations

Executive summary

1 Mobile Banking in India: Overview and

current status

1

2 Mobile Banking : SMS-based channel 10

3 Mobile Banking : USSD channel 12

4 Mobile Banking : Application based

channel

16

5 Mobile Banking :Technical solutions and

way forward

18

6 Summary of recommendations 21

Annex-I List of members 26

Abbreviations

ATM Automated Teller Machine

BC Business Correspondents

CBS Core Banking System

CDMA Code Division Multiple Access

DFS Department of Financial Services

DoT Department of Telecom

DTH Direct-To-Home

GPRS General Packet Radio Service

GSM Global System for Mobile Communication

IDRBT Institute for Development and Research in Banking Technology

IFSC Indian Financial System Code

IMG Inter-Ministerial Group

IMPS Immediate Payment Service (NPCI)

IVR Interactive Voice Response

MMID Mobile Money Identifier ( It is a seven digit number having first four

digits as bank code and remaining three as random number)

MPFI Mobile Payment Forum of India

M-PIN Mobile PIN

NFS National Financial Switch

NPCI National Payments Corporation of India

OTA Over the Air

OTP One Time Password

PAN Permanent Account Number

PSS Payments and Settlements Systems

QOS Quality of Service

RTGS Real Time Gross Settlement

SIM Subscriber Identity Module

SMS Short Messaging Service

STK SIM Application Tool Kit

MNO Mobile Network Operators

TRAI Telecom Regulatory Authority of India

UIDAI Unique Identification Authority of India

URL Universal Resource Locator

USSD Unstructured Supplementary Service Data

VAS Value Added Services

WAP Wireless Application Protocol

Executive Summary and key recommendations

1.The developments in mobile telephony, as also the mobile phone density in the

country, with over 870 Mn subscribers, presents a unique opportunity to leverage the

mobile platform to meet the objectives and challenges of financial inclusion. By

harnessing the potential of mobile technology, large sections of the un-banked and

under-banked society can be empowered to become inclusive through the use of

electronic banking services.

2. Dr. Raghuram Rajan, on taking over as Governor, Reserve Bank of India (RBI) on

September 4, 2013, had stated that there was substantial potential for mobile based

payments and that a Technical Committee would be set up to examine the options /

alternatives, including the feasibility of using encrypted SMS-based funds transfer

utility, for expanding the reach of mobile banking in the country. Accordingly, a

Technical Committee was constituted by the Reserve bank of India under the

Chairmanship of Shri B. Sambamurthy, Director, Institute for Development and

Research in Banking Technology, to study in-depth the present challenges faced in

mobile banking, the adoption of particular technologies to meet the requirements of

banks as well as vast numbers of mobile users and draw up a road-map for

implementation of the solutions.

3. During its deliberations, the Committee examined the present challenges faced by

banks for greater adoption of mobile banking as also the issues faced in enabling

greater access to the USSD channel by banks. It is pertinent to indicate here that the

Committee considered these challenges with specific reference to millions of

financially excluded populace of the country having no access to formal financial

services, and recommended certain mobile banking solutions, such as multilingual

USSD and IVR access channel, STK based common mobile banking application,

etc., keeping this segment in mind. Another pertinent point to note is that user of

mobile banking services is referred in this Report as “customer” – present and future

-, both of banks and MNOs in the same breath.

4. The Report is divided into six chapters which include Overview of mobile banking,

the SMS based channel, the USSD channel, the Application based channel,

Technical solutions and the way forward and finally the Recommendations. Some of

the recommendations are given below:

(i) Banks need to explore other means of facilitating customer/user

registration process for mobile banking which does not require a visit to the

bank branch. The potential of inter-operable ATM networks and business

correspondent arrangements has to be effectively harnessed towards meeting

this objective. Committee felt that standardization is required in (a) User

registration for mobile banking, (b) User authentication process, and (c) User

interfaces. Recognising the crucial role that customer/user awareness plays in

adoption of any technology for financial transactions as well as the need for

optimal utilization of resources, the Committee is of the opinion that joint

customer education programs by banks will go a long way in facilitating usage

of mobile banking.

(ii) Mobile Network Operators (MNOs) need to see a business model in it for

themselves and play out their role in ensuring mobile banking reaches its full

potential by cooperating with banks in their endeavor to provide the

appropriate technology / channel to the targeted users. Mobile banking can

result in customer stickiness and reduce churn for MNOs. Mobile banking can

increase revenue to MNOs and reduce costs to banks. The current solutions

already provided by banks and various technological alternatives available

can be put in place through a concerted effort between banks and telecom

service providers.

(iii) Common mobile banking applications and common technological

platforms need to be built for reaping the benefits of “network effects”. While

bank-specific applications and individual platforms have a major role in

building brand loyalty, an alternate uniform/common platform, interoperability

and similar seamless transactional experience to the users/customers of all

banks would encourage mobile banking.

(iv)The Government of India can explore the options of offering fiscal

incentives / economic subventions to the stakeholders in order to ensure

participation of various players to offer the solutions recommended here in

this Report. The committee would like to draw attention to similar law “Lei Do

Bem” (Law of the Goods)

1

enacted by Brazil in Oct 2013 which mandates that

smart phones give visibility to Brazilian made apps by either pre-loading

phones with these homegrown apps or providing a dedicated marketplace on

smart phones to display them. Similar intervention in India can support and

incentivise the relevant stakeholders to either "pre burn" common mobile

banking application on mobile handsets / SIM cards or send "over the air"

using dynamic STK to facilitate financial transactions. This is a “build-it-they-

will-come” approach.

5. Further important and key recommendations made in the report are listed below.

The approach is to offer a “product in a box” that covers the entire process of SIM

card registration, enrolment, authentication until the customer begins to use mobile

banking.

a) The customer may not be required to visit the bank branch for mobile number

registration. Alternate channels for mobile number registration may be made

available, such as interoperable ATM network across banks as well as the BC

1

http://thenextweb.com/la/2013/11/11/legislating-innovation-brazil-good-law-much/

/ agent network using biometric authentication, so that the customer can

register the mobile number conveniently.

b) The process of M-PIN generation may also be simplified and standardized

without necessitating a visit to the bank branch by the customer, so that the

customer can be on-boarded in an easy manner and start transacting using

mobile payments, and reduce barriers to entry.

o The customer may be able to set and change his M-PIN from the

handset itself using authentication parameters defined by the banks

permissible by their security guidelines.

o The customer may have the facility to set or change the M-PIN from at

least one additional channel (apart from mobile handset itself as

mentioned in point a above) such as Phone Banking, IVR, ATM,

Internet Banking.

c) Banks may implement multiple channels (application, SMS, USSD etc.) for

mobile banking so that options are available to all types of customers with any

type of handsets with suitable level of security.

d) For better authentication of the transaction by the bank, MNOs could facilitate

the mobile banking transaction by providing the mobile number from where

transaction is originated when customers transact using mobile banking

application (Currently the mobile number in the header is suppressed).

e) For facilitating funds transfer using mobile banking, the remitting customer

may be facilitated to effect person-to-person funds transfer using just the

mobile number and bank or just the Aadhaar number of beneficiary.

f) Customer may be able to make merchant payment using just his mobile

number and M-PIN/OTP on the merchant interface. The M-pin can be only

interfaced on acquiring bank’s interface such as USSD, Application etc. for

security reasons. The merchant based interfaces can accept OTP (One-Time

Password) for authentication.

g) Every bank may offer OTP services on SMS request with the standard syntax

of SMS such as “MOTP XXXXXX” to the short or long code. (XXXXXX – last 6

digits of the account number). This will help to expand the use of OTP in

mobile payments.

h) Limit of unsecured transaction (without end to end encryption) may be raised

from the existing Rs.5000/- to Rs.10000/- subject to having certain velocity

checks at the bank side. The banks may take the decision of limit

enhancement depending on their security policy and internal risk

management control measures.

i) To overcome the challenges faced by each bank in tying up with a large

number of MNOs, and to facilitate the reach and usage of mobile banking

through USSD, there is a need for common USSD gateway for mobile

banking. A common USSD Gateway based mobile banking service offers an

opportunity to provide convenient, cost effective and user friendly payment

option for all customers and thus a very convenient mechanism for banks for

furthering financial inclusion objectives of Government of India.

j) Banks and MNOs may initiate pilots using white-label multi – bank STK

application which can be distributed using application on SIM that allows SMS

encryption. Customers, merchants, agents of any bank can transact through

this interface.

k) MNOs may support,

o Application loading on new SIMs – Single mobile banking application

may be made available all new SIMs which uses encrypted SMS for

transaction processing.

o Application loading on existing SIMs – Single mobile banking

application may be made available across all existing SIMs in SMS

encrypted environment through dynamic STK and the common mobile

banking application can be pushed over-the-air.

l) The large corporates, third party players and MNOs, handset manufacturers /

resellers may initiate pilot programs to develop the single multi-bank mobile

banking applications which can use published public keys of the banks /

banks’ agents for encryption. The common application may be developed by

reputed organizations having successful track record in this field.

m) Similarly, the common application may be pre-loaded in the handset – the

mandate to be issued by Govt. of India to all handset manufacturers /

resellers in India. Handset manufacturers to burn the application on all new

handsets.

n) The committee feels for effective and efficient implementation of providing

mobile banking facilities to the customers it is imperative that the banks staff

is well versed and thoroughly trained in various aspects of the mobile banking.

For this workshop may be conducted for top officials including the chief

executive of the banks; training program may be conducted during induction

programs and probationary officer courses. Banks may also periodically

conduct refresher courses to ensure staff is abreast with latest developments

in these fast paced technology areas in mobile banking.

o) The committee also feels banks must continue to invest in handholding and

educating customers to increase the awareness of various aspects of mobile

banking. Banks collectively may invest in marketing and advertising for

widespread promotion of mobile banking.

Acknowledgements:

The Committee is thankful to all subject matter experts and others who made

presentations before the members to brief them of their view points and indicate the

general direction and path ahead for mobile banking. The Committee feels privileged

and grateful to have had presentations made by Prof. Ashok Jhunjhunwala of IIT,

Madras, Chairman of MPFI, Shri Rajesh Bansal of UIDAI, Shri Patrick Kishore, Prof.

V.N. Sastry, Dr. N. Raghu Kisore from IDRBT and representatives of various

stakeholders in the ecosystem. The Committee is thankful to Shri Suresh Sethi from

Vodafone and Shri Ram Rastogi and Shri Dheeraj Bharadwaj both from NPCI for

their active participation in the deliberations. Finally, the Committee would like to

place on record their appreciation of the secretarial and editorial support provided by

Ms. Radha Somakumar, DPSS, RBI in ensuring early completion of this Report.

Technical Committee on Mobile Banking - Report

Page 1 of 26

Chapter 1

Mobile Banking: Overview and Current status

Introduction:

1. The Payment and Settlement Systems Act, 2007 empowers the Reserve Bank of India to

authorize and regulate entities operating payment systems in the country. The Vision

Document for Payment and Settlement Systems of the RBI has, over a period of time, placed

importance on the move towards electronic payments and thereby a ‘less-cash’ society.

Towards this end, the Bank has been promoting and nurturing the growth of various modes of

electronic payments including the prepaid payment instruments, card payments, mobile

banking etc.

2. The Payment Systems Vision Document 2012-15

1

, reflects the commitment towards

provision of safe, efficient, accessible, inclusive, interoperable and authorised payment and

settlement systems in the country. The performance indicators of various payment system

segments show that, during 2012-13 the share of paper-based instruments in the volume of

total non-cash transactions has been lower than that of electronic payments. In addition to the

growth in volume as well as value processed by RTGS, the retail electronic segment too has

registered a significant growth of 35.2 percent in volume and 54.9 percent in value. Though

overall volume of transactions in mobile banking is low, there has been significant growth in

the volume this year as compared to previous years.

Mobile banking: Regulatory framework and current status

3. Recognising the potential of mobile as a channel for offering financial services in the

country, the Reserve Bank issued the first set of guidelines on mobile banking in October

2008

2

. The bank-led model was considered suitable for the country with a mandate to banks

such that all transactions should originate from one bank account and terminate in another

bank account. At this time, a few banks had already started offering information based

services like balance enquiry, stop payment instruction of cheques, transactions enquiry,

location of the nearest ATM/branch etc. through this medium.

4. The guidelines issued by RBI in October 2008, permitted banks to facilitate funds transfer

from one bank account to another bank account, both for personal remittances and purchase

of goods and services. Banks were directed on the regulatory/supervisory issues, registration

of customers for mobile banking, to ensure technology standards, interoperability, interbank

1

RBI Payment System Vision Document (2012-15) - http://www.rbi.org.in/scripts/PublicationVisionDocuments.aspx?Id=664

2

Mobile Banking Transactions in India – Operative Guidelines for Banks - http://www.rbi.org.in/scripts/NotificationUser.aspx?Id=6387&Mode=0

Technical Committee on Mobile Banking - Report

Page 2 of 26

clearing and settlement arrangements for fund transfers, customer grievance and redressal

mechanism and transaction limits in an attempt to ensure safe, secure transfer of funds.

5. Under extant regulatory prescriptions, there is no monetary restriction on fund transfer

effected through mobile banking as it is left to the risk perception of each bank and policies

approved by their respective Boards. However, end-to-end encryption for transactions in

excess of Rs. 5000/- has been mandated by RBI. Similarly, mobile as a channel for funds

transfer from a bank account for cash payout to a beneficiary who does not have a bank

account at ATMs/BCs- Rs 10,000 per transaction with a cap of Rs 25,000/-per beneficiary has

also been permitted by RBI (under the Domestic Money Transfer guidelines).

6. In line with these guidelines, banks have been offering mobile banking services to their

customers through various channels such as SMS, USSD channel, mobile banking

application etc. However, real time inter-bank mobile banking payments has been facilitated

through the setting up of the Interbank Mobile Payment Services (IMPS), now termed as

Immediate Payment Service, and operated by the NPCI with the approval of the Reserve

Bank of India. The IMPS has enhanced the efficiency of mobile banking by enabling real time

transfer of funds between bank accounts and providing a centralised interbank settlement

service for mobile banking transactions. The IMPS has also been enhanced to support

merchant payments using mobile phones to promote less cash society. The committee

considered options of using mobile for the merchant payments whereby the merchants on

initiating the payment request completes the transaction by accepting an OTP generated by

customer on his mobile. The committee also considered a standard and simple process to

generate OTP across all banks.

7. Under the PSS Act, the Reserve Bank has given approval for mobile banking services to

80 banks

3

, of which 64 have commenced operations. The customer base of banks who have

subscribed to mobile banking services stands at nearly 30 million as of October 2013.

8. In recent years, the mobile banking has been reflecting a growing trend (albeit the low

volumes) with the volume and value increasing by 108.5% (53.30 million in 2012-13 vis-à-vis 25.56

million in 2011-12) and 228.9% (Rs.59.90 billion in 2012-13 vis-à-vis Rs.18.21 billion in 2011-12)

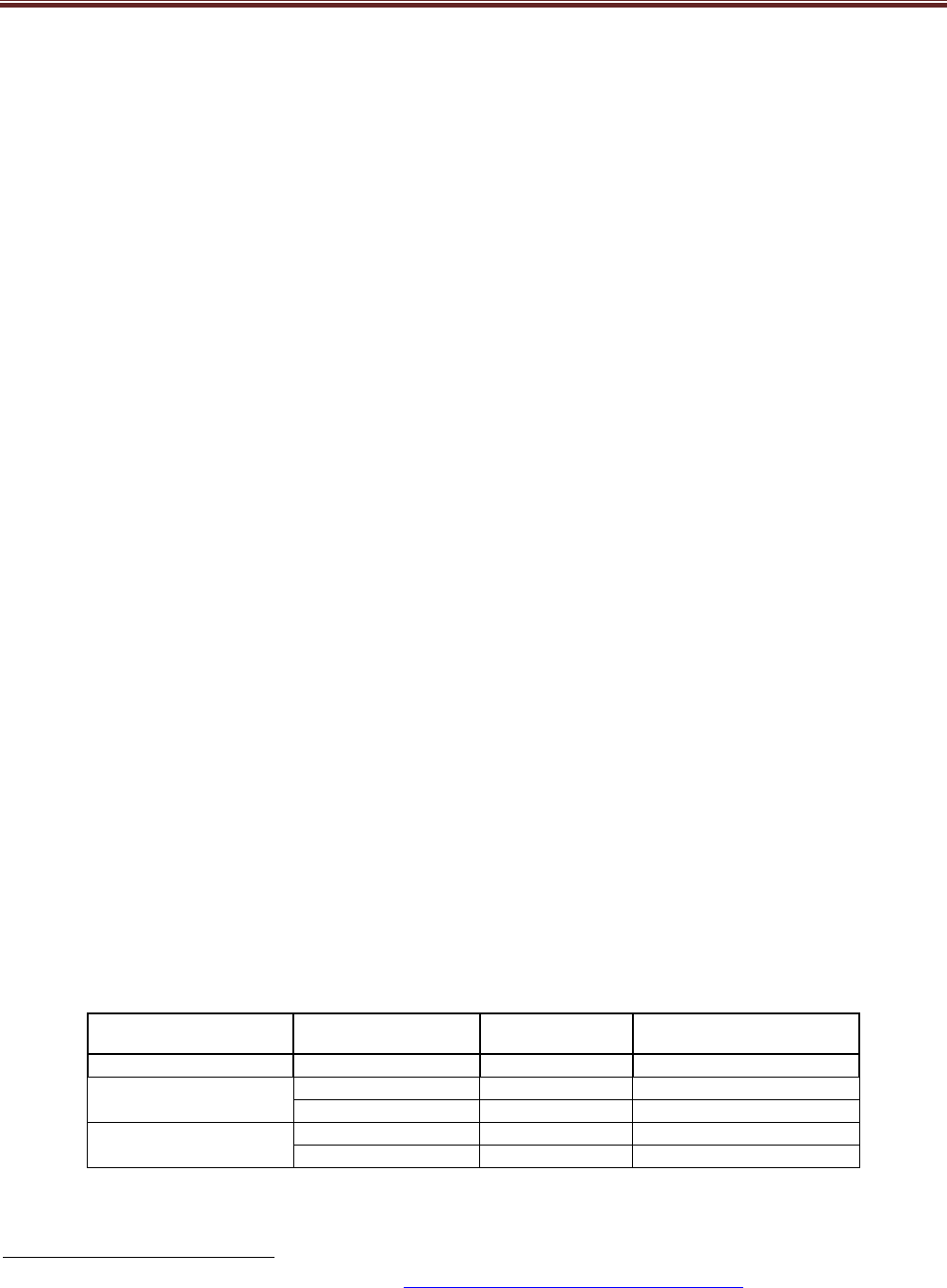

respectively. The trend in usage of Mobile Banking in the last three years is given below:

Note: figures in brackets indicate the growth over the previous year.

3

List of Banks permitted to provide Mobile Banking service in India - http://www.rbi.org.in/scripts/bs_viewcontent.aspx?Id=2463

Year

No. of Users

(Million)

Volume

(Million)

Value

(Billion Rs.)

2010-11 5.96 6.85 6.14

2011-12

12.96 25.56 18.21

(117.45%) (273.139%) (196.58%)

2012-13

22.51 53.30 59.90

(73.69%) (108.53%) (228.94%)

Technical Committee on Mobile Banking - Report

Page 3 of 26

9. Mobile telephony in India has a huge potential with 873.4

4

Mn mobile connections as on

30.06.2013 in the country, of which about 350 Mn are in rural areas. The number of

subscribers who access Internet by wireless phones has grown to about 143 Mn. With

sizeable proportion of households (41.3%) not having a bank account

5

, and large unbanked

sections of population residing in the villages (as per Census 2011, only 54.4% of rural

households had access to banking services), mobile banking offers a huge opportunity for

banking industry to leverage upon the mobile density in the country.

10. The country has a subscriber base of 870 Mn, and around 450 Mn bank accounts. The

estimates for active SIMs vary, but there are only 22 Mn active mobile banking customers. In

terms of per-transaction or per-branch costs, mobile banking transaction is economical

compared to the traditional banking channels and hence there is need for banks to encourage

the mobile banking channel in a big way keeping in mind the long term economic gains. The

committee has deliberated the ways and means to make mobile as preferred, convenient and

economical channel for accessing the banking service for all the banking customers. Put

another way,

Ø Unique mobile subscribers 350 to 550 million

6

Ø Aadhaar numbers issued 510 million

7

Ø Bank account holders 589 million

8

Ø Bank account holders using ICT based channels 182 million

Ø Number of mobile banking customers 22 million

Evidently, the large mobile subscriber base has not been leveraged for financial inclusion.

Challenges faced by banks in providing Mobile Banking to the customers

11. Despite the potential for mobile banking and the regulatory provisions enabling greater

use of mobiles as a channel for financial services in general, and for financial inclusion in

particular, banks are facing some challenges in taking mobile banking to the desired level.

These challenges are essentially in two fronts – (A) Customer enrollment related issues and

(B) Technical Issues.

A. Customer enrollment related issues are:

a) Mobile number registration

b) M-PIN generation process

4

TRAI consultation paper on ‘USSD Based mobile banking services for financial inclusion’ - http://www.trai.gov.in

5

Financial inclusion, Department of Financial Services, June 2013, website – http://financialservices.gov.in/banking/overviewofefforts.pdf

6

GSMA “The India Mobile Economy Report”, Oct 2013 http://www.gsmamobileeconomyindia.com/

7

http://pib.nic.in/newsite/PrintRelease.aspx?relid=101036

8

Crisil “ An Index to measure India’s progress on Financial Inclusion”, June 2013

Technical Committee on Mobile Banking - Report

Page 4 of 26

c) Concerns relating to security is a factor affecting on-boarding of customers

d) Bank staff education

e) Customer education

Mobile number registration

12. For a customer, in order to conduct a mobile payment transaction, his/her mobile number

needs to be registered with the bank. The process for mobile number registration is

implemented differently across banks. Currently, the process for mobile number registration

involves the following:

a) Customer mandatorily needs to go to the bank branch for most of the banks to register

his number and fill in the application form (paper-based). After verification, his number

gets registered in the CBS and in the bank’s Mobile Banking system.

b) Some leading banks have provided the facility for customer to register mobile number

at their bank’s ATMs using 2FA authentication of ATM card + ATM PIN

13. In both the above cases, the customer needs to physically go to the branch / ATM in order

to register their mobile number, which acts as a barrier in many cases, besides delaying the

entire process. Further, even where the above process of registration through ATMs is

provided, it is restricted to the use of own-bank ATMs and the same is not possible at present

by going to any other bank ATMs. The process for mobile number registration needs to be

simpler for customer to get on-boarded.

M-PIN generation

14. M-PIN is the second factor of authentication that customer needs to use in order to

conduct mobile banking transaction. Customer needs M-PIN from his respective bank in order

to get started with mobile payments. Currently, the process for M-PIN generation is

implemented differently across banks, and involves the following:

a) For most banks, after the mobile number registration at branch / any bank ATM,

customer receives M-PIN via SMS on their registered mobile number. In certain cases,

customer receives the M-PIN through postal mail.

b) Some leading banks have provided the facility for generating and changing M-PIN from

the handset itself using the mobile banking application and providing the authentication

parameters as required by the bank (e.g. Debit card details such as Debit card

number, ATM PIN, expiry date). These inputs are captured and sent through registered

mobile number, for the purpose of M-PIN generation.

c) Some leading banks have also provided the facility to generate and change M-PIN

through alternate channels such as IVR, ATM, and Internet Banking. Customer may be

able to make merchant payment using just his mobile number and M-PIN/OTP on the

merchant interface. The M-pin can be only interfaced on acquiring bank’s interface

such as USSD, Application etc. for security reasons. The merchant based interfaces

can accept OTP (One-Time Password) for authentication.

Technical Committee on Mobile Banking - Report

Page 5 of 26

d) Every bank must offer OTP services on SMS request with the standard syntax of SMS

such as “MOTP XXXXXX” to the short or long code. (XXXXXX – last 6 digits of the

account number). This will help to expand the use of OTP in mobile payments.

Concerns related to security

15. One of the major factors affecting customer on-boarding and usage of mobile banking

services is the concern relating to security of transactions effected using the mobile phone.

While mobile banking application is an end-to-end encrypted channel, the other access

channels viz. SMS, USSD, IVR, are not end-to-end encrypted. However, in order to enjoy the

higher level of security available in the application-based mobile banking, the customer’s

handset has to be GPRS-enabled.

16. Since SMS facility is available on all handsets, the issue of security can be addressed if

the SMS can be encrypted end-to-end, thus allaying any concerns relating to lack of security

in this channel.

17. In addition to this, another important aspect adding to the concerns on the part of

customers relate to how their complaints and grievances will be addressed for transacting on

this channel – whether through their bank or through their mobile service provider.

Bank staff training

18. The committee feels for effective and efficient implementation of providing mobile banking

facilities to the customers it is imperative that the banks staff is well versed and thoroughly

trained in various aspects of the mobile banking. For this workshop may be conducted for top

officials including the chief executive of the banks; training program may be conducted during

induction programs and probationary officer courses. Banks may also periodically conduct

refresher courses to ensure staff is abreast with latest developments in these fast paced

technology areas in mobile banking.

Customer education

19. The committee also feels banks must continue to invest in handholding and educating

customers to increase the awareness of various aspects of mobile banking. Banks collectively

may invest in marketing and advertising for widespread promotion of mobile banking.

B. The technical aspects which are posing a challenge relate to:

a) Access channels for transactions

b) Cumbersome transaction process

c) Coordination with MNOs in mobile banking eco-system

Access channels for transaction

20. Once the customer mobile number is registered and M-PIN is generated, customer may

use any of the access channels provided by the bank for conducting mobile banking

transactions. Currently, while most banks have provided mobile banking application and SMS

Technical Committee on Mobile Banking - Report

Page 6 of 26

facility as access channels, a few banks have also provided other access channels such as

USSD, WAP, IVR, etc. some banks also provide a combination of a few of these channels

(application + SMS, application + USSD) for offering better security.

21. Some of the issues faced in this regard are:

a) In the case of mobile banking application, the applications need to be continuously

upgraded to keep pace with newer compatible handset and operating systems.

b) In the case of SMS access channel, while it is available to all users (with all types of

handsets) for conducting mobile banking transactions, the channel is not secure end-

to-end and hence there are limits on the amounts that can be transferred using this

channel without encryption. Further, the SMS also gets stored in the ‘sent items’ of

handset, including the confidential M-PIN. The customer also needs to know the syntax

for doing any transaction through SMS.

c) As far as the USSD channel is concerned, though it is menu-driven, interactive, user-

friendly for transactions, and is available on GSM network (92.77% of the subscribers)

6

and no information is stored on the handset, the major challenge is that it is not

available to the customers on CDMA network. The USSD session per se does not offer

any additional security to the transactions other than the basic security available in the

GSM channel.

d) The IVR channel, independent of the handset can be used by all customers – it is

menu-driven, interactive and user-friendly, the information does not get stored on

handset, services can be offered in multiple languages (beneficial for financial

inclusion), the voice prompts and simple numeric inputs making it easier for customers

to adapt, etc. However, this channel is again not end-to-end encrypted and the IVR

infrastructure has to be built by the banks offering this service, thus involving cost

considerations.

e) The WAP site can be accessed by any handset provided the customer has active data

connection.

Cumbersome transaction process

22. In the present scenario, with various banks offering various channels for their customers

to undertake mobile banking transactions, the user experience is certainly not uniform across

banks / channels. The customer is required to provide different set of inputs (authentication

parameters) for each type of access channel, thus making the entire transaction process

cumbersome.

23. Currently using IMPS, for effecting a person-to-person funds transfer, the remitting

customer can provide details of the beneficiary by providing one of the three identifiers -

Mobile number and MMID of the beneficiary; IFSC + Account Number; Aadhaar Number.

Since MMID-based input required that the beneficiary should also be registered for mobile

banking with his bank, the options of IFSC+Account Number was provided to facilitate the

6

The telecommunication tariff (fifty sixth amendment) order 2013 no. 5 of 2013 www.trai.gov.in

Technical Committee on Mobile Banking - Report

Page 7 of 26

customers making inter-bank mobile transactions. From financial inclusion perspective, input

of beneficiary’s Aadhaar number has also been provided since August 2013.

24. Similarly, a merchant / enterprise, it is difficult to inform customer on how to make the

payment, since every bank process is different. Customer education is an issue because of

the above.

Coordination with MNOs in mobile banking eco-system

25. In order to offer a more secure and better user experience to their customers through their

mobile banking channels, banks need a greater level of coordination with the telecom service

providers. Some of these areas are:

a) For better authentication of the transaction by the bank, MNOs could facilitate the

mobile banking transaction by providing the mobile number from where transaction is

originated when customers transact using mobile banking application (Currently the

mobile number in the header is suppressed).

b) Greater extension of support by MNOs to all banks for providing USSD services.

c) Facilitation by the MNOs for banks to offer a more secure mobile banking to their

customers through SIM Took Kit (STK) application on SIM card for securing the mobile

banking transactions.

Recommendations

26. In order to address the above challenges, a multi-pronged approach with concerted

involvement of all stakeholders is necessary. In this context, the following solutions are

recommended for addressing the customer acquisition related challenges as well as the

technical aspects.

Recommendations for customer enrollment:

a) The customer may not be required to visit the bank branch for mobile number

registration. Alternate channels for mobile number registration may be made available,

such as ATM network across banks as well as the BC / agent network using biometric

authentication, so that the customer can register the mobile number conveniently. In

the case of first time registration of mobile number, appropriate security safeguards

may be put in place by the banks.

b) The mobile number registration process, including the registration form may be made

uniform, across all banks, so it helps with uniform customer experience. Social media

propagation of the registration process will bring more customers to this channel.

c) The process of M-PIN generation may also be simplified and standardized without

necessitating a visit to the bank branch by the customer, so that the customer can be

on-boarded in an easy manner and start transacting using mobile payments, and

reduce barriers to entry.

Technical Committee on Mobile Banking - Report

Page 8 of 26

o The customer may be able to set and change his M-PIN from the handset itself

using authentication parameters defined by the banks permissible by their

security guidelines.

o The customer may have the facility to set or change the M-PIN from at least one

additional channel (apart from mobile handset itself as mentioned in point a

above) such as Phone Banking, IVR, ATM, Internet Banking.

d) M-PIN may be generated from the registered mobile number through secure access

channels such as mobile application, SIM STK application by using authentication

parameters such as debit card credentials (debit card number, ATM PIN, expiry date)

required by bank.

e) For customers using other channels, M-PIN may be generated through bank’s phone

banking facility or IVR, or even the ATM channel, after verification of credentials (e.g.

mobile number, debit card number, ATM PIN, account number, date of birth, PAN

number, details of last transaction, etc). Further, these channels may also be offered

as additional channels to those customers who use the mobile application or SIM STK

application.

Recommendations for Technical Issues:

a) Banks may implement multiple channels (application, SMS, USSD etc.) for mobile

banking so that options are available to all types of customers with any type of

handsets with suitable level of security.

b) In case of application-based mobile banking, encrypted SMS facility may be provided

to all customers as an additional channel so as to enable them to perform transactions

in a secured manner, including high value transactions, irrespective of whether data

connectivity is available or not.

c) For facilitating funds transfer using mobile banking, the remitting customer may be

facilitated to effect person-to-person funds transfer using just the mobile number and

bank or just the Aadhaar number of beneficiary.

d) Customers may be enabled to use mobile banking service through the use of a single

or common USSD number / SMS short/long codes / IVR number / mobile application

across all banks. This will facilitate easier customer education and uniform transaction

process across all banks.

e) Limit of unsecured transaction (without end to end encryption) may be raised from the

existing Rs.5000/- to Rs.10000/- subject to having certain velocity checks at the bank

side. The banks may take the decision of limit enhancement depending on their

security policy and internal risk management control measures.

f) For better authentication of the transaction by the bank, MNOs could facilitate the

mobile banking transaction by providing the mobile number from where transaction is

originated when customers transact using mobile banking application (Currently the

mobile number in the header is suppressed).

Technical Committee on Mobile Banking - Report

Page 9 of 26

The recommendations for other issues relating to USSD and SIM Tool Kit are dealt with in

detail in subsequent chapters.

Technical Committee on Mobile Banking - Report

Page 10 of 26

Chapter 2

Mobile Banking : SMS based channel

Introduction

1. SMS is a popular and widely used channel in mobile phones. It is ubiquitously available in

all handsets irrespective of make and model and also GSM and CDMA enabled handsets.

Most customers are very conversant with the SMS channel and use the same for various

services including the short messaging. Many popular mobile VAS services such as Cricket,

Jokes, Horoscopes, etc. are based on SMS and used widely by customers.

Current status of SMS-based mobile banking

2. Given the advantages offered by SMS channel, many banks have offered mobile banking

services through the SMS channel. This includes non-financial services such as Balance

Enquiry, Mini statement, Cheque Book Request, Transaction Alerts, etc., and financial

services such as funds transfer, mobile / DTH recharge, Bill payments, etc.

3. In order to avail mobile banking services over SMS, customer needs to send the request

with a keyword and parameters to SMS short code or long code number, for e.g. for Balance

Enquiry, customer can send SMS BAL to 5667766 (short code) or 9212167766 (long code).

The request is sent to the respective bank server, and customer receives the response via

SMS. Similarly in order to perform funds transfer using the IMPS platform, customer can send

SMS “IMPS <Beneficiary account number> <Beneficiary IFSC> <Amount> <M-PIN>

<Remarks>” to bank short code or long code. The request is forwarded to the bank server,

the bank server processes the transaction, and sends response to customer via SMS.

Challenges faced

4. Following are some of the challenges faced with SMS channel for mobile banking by the

banks:

a) Customer needs to know the exact syntax of SMS for performing transaction.

b) The syntax becomes complex when (i) bank adds more transactions which will end up

as different keywords and (ii) when more input parameters are needed to complete the

transaction. Under these conditions, it is also difficult to communicate and educate the

customer to use the syntax.

c) The SMS channel is not end-to-end encrypted without having an application on the

handset to encrypt the entire SMS. There is a transaction limit as per RBI mobile

banking guidelines, of Rs 5,000/-

7

per transaction without end to end encryption.

7

Mobile Banking Transactions in India – Operative Guidelines for Banks - http://www.rbi.org.in/scripts/NotificationUser.aspx?Id=6387&Mode=0

Technical Committee on Mobile Banking - Report

Page 11 of 26

d) The SMS remains in the readable form within the sent items on the mobile phone. In

case the custody of the customer’s handset is obtained, will result into the risk of losing

the confidential information to initiate the financial transactions.

e) The SMS short code or long code for sending SMS transactions is different for each

Bank, and needs to be communicated to customer

Because of above challenges, the SMS based mobile banking has not picked up adequately,

despite the advantages offered by SMS channel.

Recommended solution for SMS based mobile banking channel

5. The solution as envisaged to resolve the above issues is to use the common mobile

banking application which will enable the use of encrypted SMS messages for mobile banking

transactions:

a) The common mobile banking application preferably using STK (SIM Tool Kit)

application for mobile banking.

b) This common application may be standard menu-driven and interactive, and can be

used by all banks so that users can perform transactions conveniently without the need

to remember or know the SMS syntax.

c) The STK application encrypts the SMS before sending, so as to ensure end-to-end

security, and can be used for transactions of higher values.

d) User does not need to know the SMS short code or long code number, the STK

application will encapsulate that information and send encrypted SMS to pre-defined

number.

Common STK application architecture

The detailed description of the infrastructure requirements for the common STK solution is

given the subsequent chapter on technical solutions.

Technical Committee on Mobile Banking - Report

Page 12 of 26

Chapter 3

Mobile Banking-USSD based channel

Introduction:

1. Unstructured Supplementary Service Data (USSD) is a protocol used by GSM cellular

telephones to communicate with the telecom service provider's systems. USSD can be used

for WAP browsing, prepaid callback service, mobile-money services, location-based content

services, menu-based information services, and as part of configuring the phone on the

network.

2. USSD messages are up to 182 alphanumeric characters in length. Unlike Short Message

Service (SMS) messages, USSD messages create a real-time connection during a USSD

session. The connection remains open, allowing a two-way exchange of a sequence of data.

This makes USSD more interactive and advantageous than services that use SMS.

Advantages of USSD:

3. The USSD platform which is MNO dependent can be efficiently used by the mobile banking

platforms due to the following advantages:

a) USSD works on all GSM phones irrespective of make, model or service provider –

thus all phones including low end phones are capable of handling this.

b) It does not require any application/software to be downloaded to the handset.

c) It is interactive in nature – and thus enables complex transactions as well which

may not be possible through SMS.

d) It is a session based communication i.e. it does not store any data on the phone

and transaction terminates as the session end.

e) USSD utilizes the same capability as the voice calls hence has the coverage most

of the parts of the country having GSM voice call coverage.

f) It is safer and much faster than traditional SMS based transactions (recent TRAI

guidelines on Quality of Service indicates two seconds as acceptable response

time requirement for the USSD session

8 9

).

g) It can support multiple languages which is very useful for effective financial

inclusion roll out.

Current

Status of USSD Implementation

4. Realizing the benefits and potential of USSD based mobile banking, some of the banks

have launched USSD based mobile banking services e.g. State Bank of India, Canara Bank,

ICICI Bank, with the help of telecom aggregators who in turn have tied up with few MNOs. For

8

TRAI – The Mobile Banking (Quality of Service) (Amendment) Regulations, 2013 (13 of 2013) dated 26

th

Nov 2013 -

http://www.trai.gov.in/Content/RegulationUser.aspx?id=0&qid=3

9

TRAI – The Mobile Banking (Quality of Service) Regulations, 2012 (8 or 2012) dated 17

th

April, 2012 -

http://www.trai.gov.in/Content/Regulation_Version.aspx?REG_ID=111&id=0&qid=0

Technical Committee on Mobile Banking - Report

Page 13 of 26

instance, ICICI Bank has tied up with Idea, Aircel, Tata Docomo, Reliance and MTNL for

offering USSD platform to its customers on their GSM network.

5. National Payments Corporation of India (NPCI) has implemented the common USSD

gateway with the single short code *99# to offer the USDD channel of mobile banking for all

banks. Even though a large number of banks are participating in the common USSD gateway,

only two MNOs are operational which is limiting the use of the services being extended to all

bank customers.

TRAI regulations and initiatives on USSD channel to be available for mobile banking

6. The Inter-Ministerial Group (IMG) was constituted on November 19, 2009 to work out the

relevant norms and modalities for introduction of mobile based delivery model for delivery of

basic financial services and to enable finalization of a framework to allow financial

transactions using mobile phones.

7. The IMG had, among other things, recommended that TRAI may draw up guidelines to

ensure high availability of associated communication services in mobile banking. Accordingly,

based on a consultation with stakeholders, TRAI had issued the Mobile Banking (QOS)

Regulations, 2012 on April 17, 2012. Broadly, these regulations mandated that the access

providers (telecom companies) shall, among others, (a) facilitate banks to use SMS, USSD

and IVR to provide banking services to its customers (b) deliver the message generated by

the bank or the customer within the time frame specified (within the response time of less

than 10 seconds for SMS, IVR, WAP and STK, and in less than 2 seconds for USSD); the

expiry time for SMS was stated to be 72 hours (c) ensure that the customer is able to

complete the transaction in not more than two stage transmission of the message in all cases

(d) maintain the record of mobile banking messages for six months for audit purposes.

8. Subsequently, the above regulations were extended (on November 26, 2013) to include

authorized agents of banks acting as the aggregation platform providers to use SMS, USSD

and IVR to provide banking services. Similarly, since it was realized that completion of

transaction in two stages may not be possible for every kind of transaction on a mobile

banking menu, the matter was examined and TRAI has increased the completion stages to

five stages (from the earlier two stages).

9. The IMG framework envisages opening of the mobile-linked ‘no-frills’ accounts, which

would be operated using mobile phones and the customer would be able to perform five basic

transactions – cash deposit, cash withdrawal, balance enquiry, transfer of money from one

mobile-linked account to another, and transfer of money to a mobile-linked account from a

regular bank account.

10. The mobile banking ecosystem comprises of two distinct sectors – the financial services

sector and the telecom sector – both of who are governed by two separate sets of

regulations. In order to make financial transactions available for the unbanked population,

Technical Committee on Mobile Banking - Report

Page 14 of 26

USSD-based mobile channels can be effectively deployed, as has already been launched by

certain banks like SBI, Canara Bank, ICICI Bank in partnerships with some telecom service

providers.

11. The final outcome is that TRAI

10 11

has mandated that a pay-per-use charge within the

ceiling tariff of Rs.1.50 per USSD session would be payable by the subscriber upon

establishment of an outgoing USSD session, regardless of whether the session results in a

successful or a failed banking transaction.

Recommendations: The way forward for USSD

12. The USSD channel based offering of mobile banking services may take following paths in

future:

Bank-specific USSD offering

13. The recent TRAI guidelines, it is open to banks to tie up with MNOs to offer these

services directly to their customers by getting into arrangements with each of the MNOs. This

may be done by the bank with each of the MNO or their service providers. With this, the

customer dialing the USSD code will reach the bank’s own menu, and the transactions will be

routed to the bank directly by MNO. However, in such cases, this facility is extended only to

bank customers who are also the subscribers of those MNOs with whom the bank has tied up

for USSD channel.

Implementation of common USSD gateway for mobile banking

14. To overcome the challenges faced by each bank in tying up with a large number of

MNOs, and to facilitate the reach and usage of mobile banking through USSD, there is a need

for common USSD gateway for mobile banking. A common USSD Gateway based mobile

banking service offers an opportunity to provide convenient, cost effective and user friendly

payment option for all customers and thus a very convenient mechanism for banks for

furthering financial inclusion objectives of Government of India.

15. The committee also recommends that the implementation of the TRAI regulations must be

expedited by all the stakeholders.

Benefits of a common USSD gateway

16. It will offer a common platform for all banks thus eliminating the need for banks to

establish individual infrastructure for this channel. Common USSD short code e.g. *99# can

be used by customers, merchants, and agents for performing mobile banking transactions.

17. Customers can avail following standard menu and transaction services through common

USSD gateway to perform operations such as generation and changing the M-PIN, person to

10

TRAI Press Release on Tariff for USSD and Mobile Banking (Quality of Service) Regulations, 203 -

http://www.trai.gov.in/WriteReadData/WhatsNew/Documents/PR%20%20-%20USSD%20based%20mobile%20banking%20services-New26112013.pdf

11

TRAI – The Telecommunication Tariff (Fifty Sixth Amendment) Order, 2013 dated 26

th

Nov 2013 -

http://www.trai.gov.in/Content/RegulationUser.aspx?id=0&qid=2

Technical Committee on Mobile Banking - Report

Page 15 of 26

person funds transfer transactions as well as merchant payments, other banking services

such as Balance Enquiry, Mini Statement, Cheque Book Request, etc., value added services

such as Mobile top-up, DTH top-up, Bill Payments etc., other transactions including OTP

Generation, Mandate Creation etc.

18. The merchants can also benefit from initiating USSD payment message to receive

payments from customer (using just customer mobile number and bank) on common USSD

platform

Common USSD gateway architecture

Technical Committee on Mobile Banking - Report

Page 16 of 26

Chapter 4

Mobile Banking-Application based

Introduction

1. All banks who have received the approval from RBI for mobile banking are offering the

application-based mobile banking channel to their customers. Customers can download the

mobile banking application and perform variety of services including the following:

a) Non-financial transactions such as Balance Enquiry, Mini statement, Cheque Book

request

b) Financial transactions such as Funds transfer, mobile / DTH recharge, bill payments,

etc

2. The mobile application is offered on various platforms such as Java, Symbian, Blackberry

OS, Windows, Android, Apple iOS, etc. Many Banks have made the mobile application

available in the app stores such as Google, Apple, Blackberry, etc for easy search and

download by the customers.

Advantages of the application based mobile banking

3. Following are the advantages of the application based mobile banking,

a. Applications once downloaded are easy to use for the customers who are proficient

in using the smart phone based applications.

b. Banks have made these applications compliant with most of the latest operating

systems covering the large range of smart phones in use.

c. It has been experienced by the banks that once customer has used the application-

based mobile banking, he continues to use the same unless there is a change of

the handset and/or mobile number.

d. The application-based mobile banking can also communicate using SMS and

GPRS (Data) channels with the mobile banking system of the bank.

Challenges faced of the application based mobile banking

4. Following are some of the challenges faced with application-based channel for mobile

banking by the banks:

a) Banks need to develop and test the application on the variety of handsets and

operating system version combinations (in excess of 1,000 combinations). It is

very difficult for banks to develop, test and roll out such an initiative for mobile

banking services

Technical Committee on Mobile Banking - Report

Page 17 of 26

b) Customer needs to have compatible handset for download and installation of

mobile application which is normally communicated to the customers by means

of bank website

c) Customer needs to have GPRS subscription in order to download application

and perform transactions

d) In case of any enhancement or change, customer needs to upgrade the

application

Because of the above challenges, the application-based mobile banking has not picked up

to the desired levels.

Recommended solution

5. Following are some of the recommended solutions

a. Common application for mobile banking may be standardized across all banks

and having minimum required transaction set for all banks. This would also

facilitate in educating the bank customers.

b. Mobile banking application may allow transaction over SMS, USSD and GPRS

channels also. (The mobile banking application may encrypt the SMS before

sending, so that it is end-to-end secure, even for transaction of higher value.)

c. This application can be used by any user (customers, merchants, agents)

irrespective of the bank with which they have an account

6. Customers can avail the standard menu and transaction services through common mobile

application which includes operations such as Generation and changing M-PIN, person to

person funds transfer using only mobile number, banking services such as Balance Enquiry,

Mini Statement, Cheque Book Request, etc., merchant payments, value added services such

as Mobile top-up, DTH top-up, Bill Payments etc.

Benefits of Common mobile application

7. All the challenges in point 4 above can be overcome by common mobile banking

application

Recommendations – Application based mobile banking

8. The Common mobile application may be developed and distributed (refer chapter 5) which

may have standard common menu containing the minimum and most required transaction

set.

Technical Committee on Mobile Banking - Report

Page 18 of 26

Chapter 5

Mobile Banking –Technical Solutions & the way forward

Introduction

1. In order to leverage upon the mobile density in the country and to make the vision of mobile

banking as a channel for financial inclusion, it is imperative to explore new and more cost

effective solutions for mobile banking. The Technical Committee formed by RBI was advised

to evaluate and analyse the options/alternatives including the feasibility of using encrypted

SMS/USSD based mobile banking.

2. The broad terms of reference of this Committee were as follows:

a) Conduct in-depth study of the challenges faced by the Banks in taking mobile banking

forward to desired level

b) Study the challenges faced by banks in introducing USSD channel and suggest

solutions, if any, to take this forward

c) Consider the advantages / challenges of having a single application across all

handsets in an SMS encrypted environment

d) Any other optimum solution that would make mobile banking ubiquitous in the country

e) Draw up a road-map for implementation of the solutions recommended

3. There is no gain-saying the fact mobile banking is an ideal solution to accelerate financial

inclusion in terms of Availability, Accessibility and Affordability and as such it needs to be

integrated to the banks’ business and operating models. Increasing the adoption of Mobile

banking would help the objective of less cash society with huge benefits to all stakeholders.

Hence, banks ought to redesign their business and operating process to accelerate the

adoption of Mobile banking, with process change being a critical success factor. The potential

of mobile banking is of epic proportions and with right kind of investments in awareness /

education, the adoption of mobile banking would gain traction.

4. Accordingly, in line with its mandate, the committee has outlined below some of the

technical solutions which, when implemented by banks and MNOs, would facilitate faster and

effective adoption of mobile banking in the country. These technical solutions include:

a. Platform: Common USSD gateway (as explained in chapter 3)

b. STK:

i. MNOs or SIM manufacturer burning the common mobile banking

application (to be developed) in all the new SIMs to be distributed in

India.

Technical Committee on Mobile Banking - Report

Page 19 of 26

ii. MNOs transmitting the common mobile banking application over the air

(OTA) using dynamic STK facility for existing SIMs.

c. Application: Common application development and burn on the every new

handset sold in India

d. Application: Common application development and distribution by third parties

5. While the first option deals with development of a common technical platform to facilitate

connectivity between multiple banks and multiple MNOs (thus providing the benefit of network

effect to the banks’ mobile banking customers), the second options / solutions essentially deal

with the distributional aspects of the secure solution by means of STK to the end-users. The

actual development of the application could be done by any third party solution provider.

6. Following are the distribution mechanisms of the secure mobile banking application to the

customers:

STK application on Operator SIM

7. STK application can be embedded on operator SIM and can be distributed to customers by

the MNOs. Keys necessary for encryption are stored in the SIM. Transmission of data can be

either SMS or GPRS (data) channel. STK application on operator SIM can be used by any

customer, irrespective of handset. The STK application can be standard menu-driven,

interactive and user-friendly.

Advantages:

a) Supports all standard phones and SIMs

b) Secure SMS and data communication channels usage

c) Customers, merchants, BC agents of any bank can transact through this interface.

Challenges:

a) For the existing SIMs the operator needs to support the dynamic STK so that the

application can be downloaded over the air (OTA) which is technically feasible but may

be difficult for the older version of the SIM’s. The space availability on the older SIM

cards needs to be examined.

Mobile banking application: development and distribution by third parties

8. Mobile banking application can be developed and distributed to customer by trusted third

parties, MNOs and handset manufacturers / resellers. Transmission of data shall be through

SMS or GPRS channel. Banks / agents need to publish the public keys which can be used by

the third parties to encrypt the data. Keys necessary for encryption are stored in the mobile

application. The application can be simple, menu-driven, interactive, and user-friendly.

Technical Committee on Mobile Banking - Report

Page 20 of 26

9. The mobile application (multi-bank application) can be developed and distributed by large

corporates, third party players, MNOs and handset manufacturers / resellers. MNOs can burn

the STK in the new SIMs with common mobile banking application or send the STK over the air for

existing SIMs provided such SIMs are technically compatible to receive such STK over the air.

10. Third parties for e.g. LIC, Railways, MNOs, handset manufacturers / resellers who provide

goods or services on credit / hire-purchase can develop and deploy such applications. They

can build value added services such as reminders for bill payments, and may even

advertise/cross sell for other products.

The advantages are as follows:

a) For large merchants, this shall offer uniform experience across all customers having

different banking relationship

b) Customers can use the single interface for the multiple banking relationship

c) Secure transactions and can use SMS and GPRS channels seamlessly with enhanced

transaction limits

Recommendations – Mobile banking – Technical Solutions

11. Banks and MNOs may initiate pilots using white-label multi – bank STK application which

can be distributed through application on SIM that allows SMS encryption. Customers,

merchants, agents of any bank can transact through this interface.

12. MNOs may support,

a. Application loading on new SIMs – Single mobile banking application may be made

available all new SIMs which uses encrypted SMS for transaction processing.

b. Application loading on existing SIMs – Single mobile banking application may be

made available across all existing SIMs in SMS encrypted environment through

dynamic STK and the common mobile banking application can be pushed over-the-

air.

13. The large corporates, third party players and MNOs, handset manufacturers / resellers

may initiate pilot programs to develop the single multi-bank mobile banking applications which

can use published public keys of the banks / banks’ agents for encryption. The common

application may be developed by reputed organizations having successful track record in this

field.

14. Similarly, the common application may be pre-loaded in the handset – the mandate to be

issued by Govt. of India to all handset manufacturers / resellers in India. Handset

manufacturers to burn the mobile banking application on all new handsets.

Technical Committee on Mobile Banking - Report

Page 21 of 26

Chapter 6

Mobile Banking- Summary of Recommendations

Introduction

1. The developments in mobile telephony as also the mobile phone density in the country,

with over 870 Mn mobile phone subscribers, presents a unique leverage to meet the

objectives and challenges of financial inclusion. By harnessing the potential of mobile

penetration, large sections of the un-banked and under-banked society can be empowered to

become inclusive through the use of electronic payments. In order to address the above

challenges, a multi-pronged approach with concerted involvement of all stakeholders is

necessary. In this context, the following solutions are recommended for addressing the

customer acquisition related challenges as well as the technical aspects.

Recommendations for customer enrollment:

2. To simplify the customer adoption for mobile banking

a) The customer may not be required to visit the bank branch for mobile number

registration. Alternate channels for mobile number registration may be made available,

such as interoperable ATM network across banks as well as the BC / agent network

using biometric authentication, so that the customer can register the mobile number

conveniently. In the case of first time registration of mobile number, appropriate

security safeguards may be put in place by the banks.

b) The mobile number registration process, including the registration form may be made

uniform, across all banks, so it helps with uniform customer experience. Social media

propagation of the registration process will bring more customers to this channel.

c) The process of M-PIN generation may also be simplified and standardized without

necessitating a visit to the bank branch by the customer, so that the customer can be

on-boarded in an easy manner and start transacting using mobile payments, and

reduce barriers to entry.

o The customer may be able to set and change his M-PIN from the handset itself

using authentication parameters defined by the banks permissible by their

security guidelines.

o The customer may have the facility to set or change the M-PIN from at least one

additional channel (apart from mobile handset itself as mentioned in point a

above) such as Phone Banking, IVR, ATM, Internet Banking.

d) M-PIN may be generated from the registered mobile number through secure access

channels such as mobile application, SIM STK application by using authentication

Technical Committee on Mobile Banking - Report

Page 22 of 26

parameters such as debit card credentials (debit card number, ATM PIN, expiry date)

required by bank.

e) For customers using other channels, M-PIN may be generated through bank’s phone

banking facility or IVR, or even the ATM channel, after verification of credentials (e.g.

mobile number, debit card number, ATM PIN, account number, date of birth, PAN

number, details of last transaction, etc). Further, these channels may also be offered

as additional channels to those customers who use the mobile application or SIM STK

application.

f) Customer may be able to make merchant payment using just his mobile number and

M-PIN/OTP on the merchant interface. The M-pin can be only interfaced on acquiring

bank’s interface such as USSD, Application etc. for security reasons. The merchant

based interfaces can accept OTP (One-Time Password) for authentication.

g) Every bank may offer OTP services on SMS request with the standard syntax of SMS

such as “MOTP XXXXXX” to the short or long code. (XXXXXX – last 6 digits of the

account number). This will help to expand the use of OTP in mobile payments.

h) The committee feels for effective and efficient implementation of providing mobile

banking facilities to the customers it is imperative that the banks staff is well versed

and thoroughly trained in various aspects of the mobile banking. For this workshop

may be conducted for top officials including the chief executive of the banks; training

program may be conducted during induction programs and probationary officer

courses. Banks may also periodically conduct refresher courses to ensure staff is

abreast with latest developments in these fast paced technology areas in mobile

banking.

i) The committee also feels banks must continue to invest in handholding and educating

customers to increase the awareness of various aspects of mobile banking. Banks

collectively may invest in marketing and advertising for widespread promotion of

mobile banking.

(It is proposed that above recommendations may be acted upon within 6 to 12 months)

Recommendations for Technical Issues:

3. To address the technical issues the following course of action is recommended

a) Banks may implement multiple channels (application, SMS, USSD etc.) for mobile

banking so that options are available to all types of customers with any type of

handsets with suitable level of security.

b) In case of application-based mobile banking, encrypted SMS facility may be provided

to all customers as an additional channel so as to enable them to perform transactions

in a secured manner, including high value transactions, irrespective of whether data

connectivity is available or not.

Technical Committee on Mobile Banking - Report

Page 23 of 26

c) For facilitating funds transfer using mobile banking, the remitting customer may be

facilitated to effect person-to-person funds transfer using just the mobile number and

bank or just the Aadhaar number of beneficiary.

d) Customers may be enabled to use mobile banking service through the use of a single

or common USSD number / SMS short/long codes / IVR number / mobile application

across all banks. This will facilitate easier customer education and uniform transaction

process across all banks.

e) Limit of unsecured transaction (without end to end encryption) may be raised from the

existing Rs.5000/- to Rs.10000/- subject to having certain velocity checks at the bank

side. The banks may take the decision of limit enhancement depending on their

security policy and internal risk management control measures.

f) For better authentication of the transaction by the bank, MNOs could facilitate the

mobile banking transaction by providing the mobile number from where transaction is

originated when customers transact using mobile banking application (Currently the

mobile number in the header is suppressed).

(It is proposed that above recommendations may be acted upon within 6 to 12 months)

Recommended solution for SMS based mobile banking channel

4. The solution as envisaged to resolve the above issues is to use the common mobile

banking application which will enable the use of encrypted SMS messages for mobile banking

transactions:

a) The common mobile banking application preferably using STK (SIM Tool Kit)

applications for mobile banking.

b) This common application may be standard menu-driven and interactive, and can be

used by all banks so that users can perform transactions conveniently without the need

to remember or know the SMS syntax.

c) The STK application encrypts the SMS before sending, so as to ensure end-to-end

security, and can be used for transactions of higher values.

d) User does not need to know the SMS short code or long code number, the STK

application will encapsulate that information and send encrypted SMS to pre-defined

number.

Recommendations: The way forward for USSD

5. The committee also recommends that the implementation of the TRAI regulations must be

expedited by all the stakeholders.

Bank-specific USSD offering

6. The recent TRAI guidelines, it is open to banks to tie up with MNOs to offer these services

directly to their customers by getting into arrangements with each of the MNOs. This may be

done by the bank with each of the MNO or their service providers. With this, the customer

dialing the USSD code will reach the bank’s own menu, and the transactions will be routed to

Technical Committee on Mobile Banking - Report

Page 24 of 26

the bank directly by MNO. However, in such cases, this facility is extended only to bank

customers who are also the subscribers of those MNOs with whom the bank has tied up for

USSD channel.

Implementation of common USSD gateway for mobile banking

7. To overcome the challenges faced by each bank in tying up with a large number of MNOs,

and to facilitate the reach and usage of mobile banking through USSD, there is a need for

common USSD gateway for mobile banking. A common USSD Gateway based mobile

banking service offers an opportunity to provide convenient, cost effective and user friendly

payment option for all customers and thus a very convenient mechanism for banks for

furthering financial inclusion objectives of Government of India.

(It is proposed that above recommendations may be acted upon within 12-18 months)

Recommendations – Application based mobile banking

8. The Common mobile application may be developed and distributed (refer chapter 5) which

may have standard common menu containing the minimum and most required transaction

set.

Recommendations – Mobile banking – Technical Solutions

9. Following technical solutions are recommended

a) Banks and MNOs may initiate pilots using white-label multi – bank STK application

which can be distributed using application on SIM that allows SMS encryption.

Customers, merchants, agents of any bank can transact through this interface.

b) MNOs may support,

o Application loading on new SIMs – Single mobile banking application may be

made available all new SIMs which uses encrypted SMS for transaction

processing.

o Application loading on existing SIMs – Single mobile banking application may be

made available across all existing SIMs in SMS encrypted environment through

dynamic STK and the common mobile banking application can be pushed over-

the-air.

c) The large corporates, third party players and MNOs, handset manufacturers / resellers

may initiate pilot programs to develop the single multi-bank mobile banking

applications which can use published public keys of the banks / banks’ agents for

encryption. The common application may be developed by reputed organizations

having successful track record in this field.

Technical Committee on Mobile Banking - Report

Page 25 of 26

Similarly, the common application may be pre-loaded in the handset – the mandate to

be issued by Govt. of India to (a) all handset manufacturers / resellers in India.

Handset manufacturers to burn the mobile banking application on all new handsets (b)

to MNOs requiring them to either burn the STK in the new SIMs with common mobile banking

application or send the STK over the air for existing SIMs provided such SIMs are technically

compatible to receive such STK over the air.

(It is proposed that above recommendations may be acted upon within 12-18 months)

Technical Committee on Mobile Banking - Report

Page 26 of 26

ANNEX 1

Names of members of the RBI Technical Committee for Mobile Banking

S.No.

Name

1 Mr B. Sambamurthy

Director,

IDRBT

Chairman

2 Mr Pulak Kumar Sinha

General Manager – Payment Systems,

State Bank of India

Member

3 Mr Rahul Joshi

Joint General Manager – Mobile Banking and

Payments,

ICICI Bank

Member

4 Mr Anand Rao

Vice President – Alternate Delivery Channels,

Axis Bank

Member

5 Mr Dilip Asbe

Chief Operating Officer,

National Payments Corporation of India

Member

6 Mr Anthony Thomas

Chief Information Officer,

Vodafone India

Member

7 Mr C. N. Ram

Ex - Chief Information Officer,

HDFC Bank

Member

8 Mr Pravir Vohra

Ex – President and Group – Chief Technology Officer,

ICICI Bank

Member

9 Mr Vijay Chugh,

Chief General Manager, Department of P

ayment and

Settlement Systems,

Reserve Bank of India

Member Secretary