FDIC QUARTERLY

31

1

We combine the categories of GSEs and agency- and GSE-backed mortgage pools because Financial Accounting Standards Board

Statements No. 166 and No. 167 resulted in the consolidation of a large amount of securitized loan balances back onto lender

balance sheets in first quarter 2010. Ginnie Mae mortgage pools are classified as agency- and GSE-backed mortgage pools.

2

The complete list of other financial companies is monetary authority, property-casualty insurance company, life insurance

company, private pension fund, federal government retirement fund, state or local government retirement fund, mutual fund,

ABS issuer, finance company, real estate investment trust, broker-dealer, holding company, and funding corporation.

BANK AND NONBANK LENDING OVER THE PAST 70 YEARS

Introduction In recent years, some banking activities and their inherent risks have migrated from banks

to nonbanks. While banks have increased their share of outstanding loans since the finan-

cial crisis, a significant portion of residential mortgage lending and leveraged lending has

migrated out of banks. Government-sponsored enterprises (GSEs) loosened their residential

mortgage underwriting criteria, and nonbanks markedly increased their residential mort-

gage origination and servicing, which may increase risks to the financial system.

Banks’ origination and distribution to nonbanks of a large volume of covenant-lite lever-

aged loans also have the potential to create unexpected vulnerabilities during a downturn.

Competition between banks and nonbank financial companies may affect lending standards

and strategies. Banks also have nonbank financial companies as customers, and this may

expose banks to risk in many ways.

The FDIC continues to study the changing nature of the lending market and specific sectors,

how banks are responding to the growth of nonbank lenders in certain lending areas, and

the implications of these potential risks for the banking sector and the economy. This article

provides an overview of broad trends in lending markets. The first two sections describe

the lenders that are active in the market and summarize lending from 1952 to 2018. The last

three sections discuss bank and nonbank lending in specific lending markets. Accompany-

ing articles discuss residential mortgage lending and corporate debt in more detail.

Types of Lenders and

Loan Holders

Many types of companies lend money, and some companies fund lending markets by

purchasing loans. Some companies, like banks and credit unions, originate loans and either

hold them on their balance sheets as assets or sell them to other investors. Other businesses,

such as nonbank mortgage lenders and other finance companies, tend to have more limited

balance sheet capacity and generally follow an originate-to-distribute model. These institu-

tions originate loans to sell them immediately to investors. Other investors—like life insur-

ance companies and some issuers of asset-backed securities (ABS)—do not originate many

loans but purchase existing loans from originators. Life insurance companies purchase loans

to hold as assets, while issuers of ABS buy and bundle the loans into securities, which they

sell to investors.

In this article, loan holders are grouped according to Federal Reserve Flow of Funds catego-

ries. The main categories are banks, credit unions, GSEs, issuers of ABS, other financial

companies, and nonfinancial companies. We separate banks and credit unions because their

business lines and strategies differ in some ways. GSEs are federally chartered corporations:

Fannie Mae, Freddie Mac, Federal Home Loan Banks, Farmer Mac, and the Farm Credit

System, following the definitions in the Flow of Funds for GSEs and agency- and GSE-

backed mortgage pools, unless otherwise noted. Ginnie Mae is wholly owned by the federal

government and guarantees mortgage-backed securities (MBS) backed by mortgages that are

insured by federal agencies.

1

Other financial companies include entities like finance compa-

nies, which make loans to hold or to sell; insurance companies, which tend to purchase loans

as assets; and issuers of ABS, which purchase loans to securitize them.

2

The nonfinancial

group includes the government, nonprofits, nonfinancial businesses, and households, and all

of these hold loans as assets.

2019 • Volume 1 3 • Number 4

32 FDIC QUA RTER LY

Historic Perspective of the

Lending Market

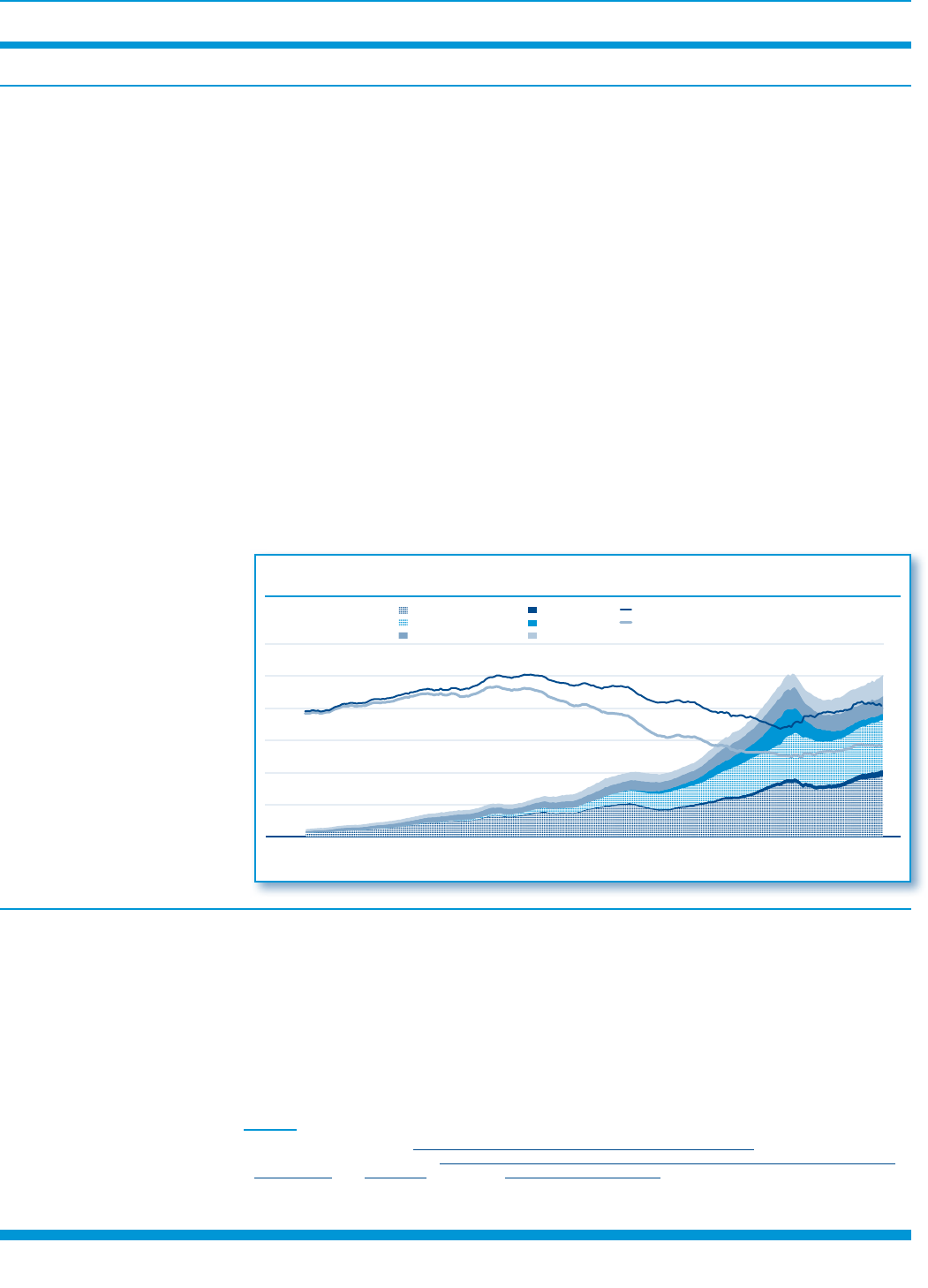

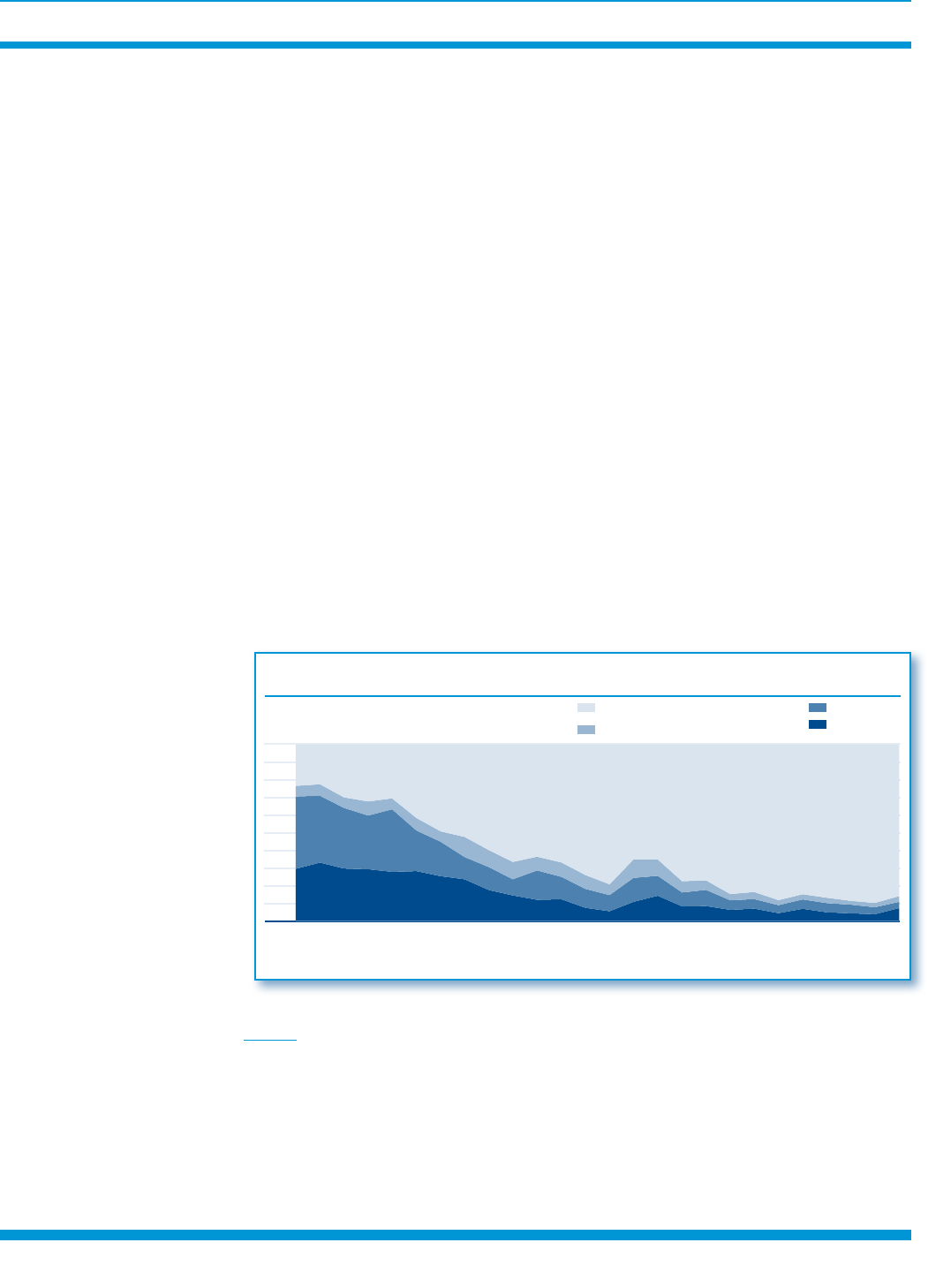

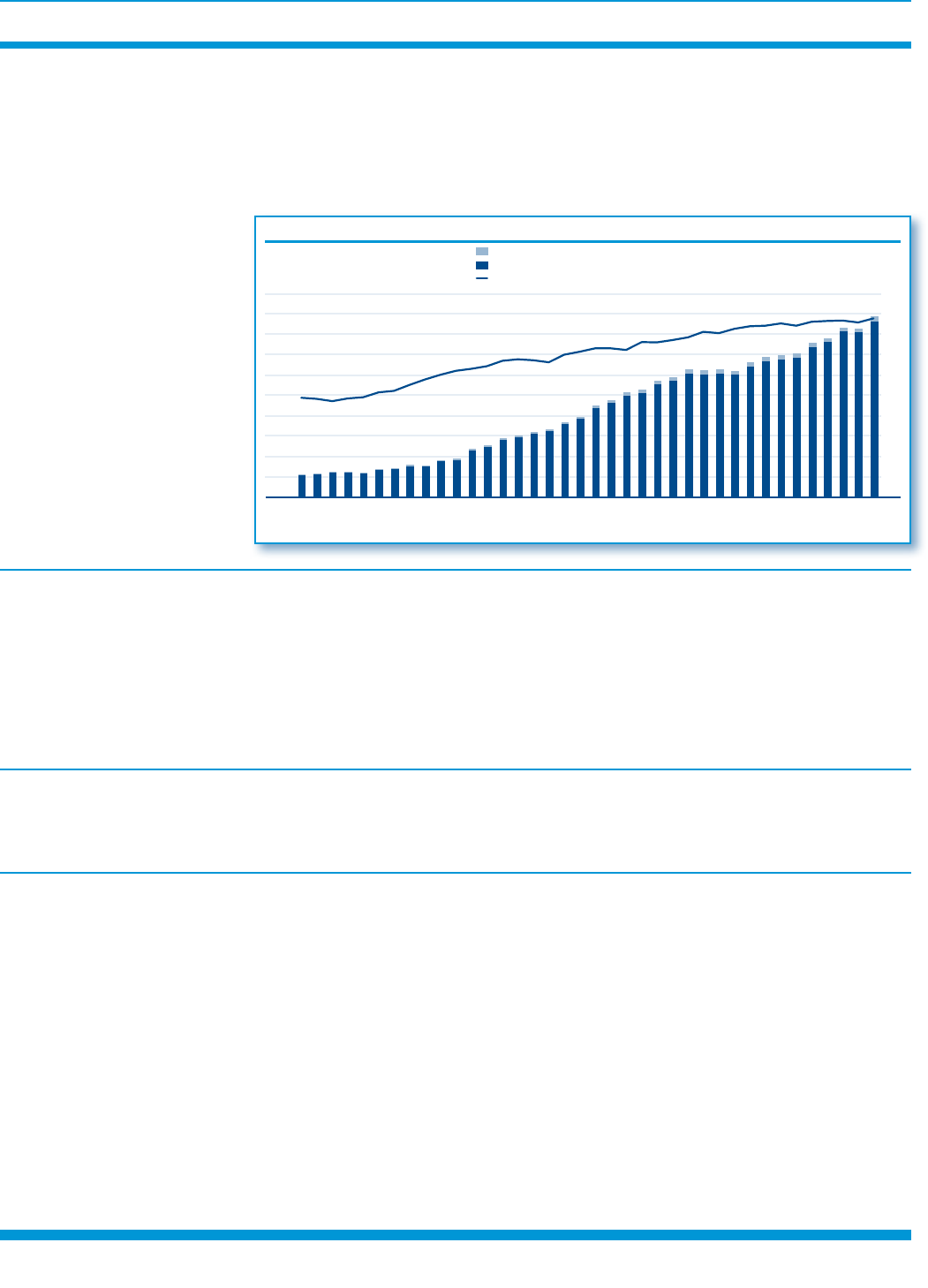

Total lending has grown dramatically since the 1950s, with the largest growth in loan hold-

ings in banks and the GSEs (Chart 1). The bank share peaked at 62percent in 1974. It then

fell fairly consistently and bottomed out in fourth quarter 2009 at 32percent. Over the same

period, corporations also shifted toward market-based financing and issued debt securities

like bonds and commercial paper. Debt securities are a significantly larger portion of nonfi-

nancial corporations’ overall debt obligations than they were in past decades. Since 2008, the

bank share of loans outstanding has increased modestly and has stabilized around 37percent

since first quarter 2016. In 2018, the total of corporate debt securities outstanding was about

twice the sum of corporate bank loans and commercial mortgages.

The shifts in bank lending also reflect the growth of nonbank loan holders, primarily in the

mortgage market. GSEs hold an increasing share of residential mortgages. The growth of

mortgage securitization played a major role in the shift (see accompanying article, “Trends

in Mortgage Origination and Servicing: Nonbanks in the Post-Crisis Period”). GSEs were

created to serve as a secondary market for residential mortgages by purchasing mortgages

from originators.

3

This allowed originators to make more loans. In the 1970s, Fannie Mae and

Freddie Mac began securitizing the mortgages they had purchased into MBS, which contrib-

uted to the growth of the secondary market for mortgages. The rise of securitization enabled a

broader range of investors to fund the mortgage market, generating growth in mortgages held

by the GSEs. In second quarter 2019, the GSEs held about 31percent of all loans outstanding.

From the 1980s to about 2005, the bank share of non-GSE loans fell and then recovered, with

a more pronounced rebound since the financial crisis that started in 2007.

e Bank Share of Loans Fell in the 1980s and 1990s as Securitization Developed,

but Started Rising Aer 2009

Source: Federal Reserve Flow of Funds (Haver Analytics).

Note: Dollar values are adjusted for ination.

Loans Outstanding

$ Billion 2012

0

5,000

10,000

15,000

20,000

25,000

30,000

1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012 2017

Banks Credit Unions

GSEs and Agency Pools Issuers of ABS

Other Financial

Nonnancial

Bank Share of Loans

Percen

t

0

10

20

30

40

50

60

70

80

Bank Share of Loans

Bank Share of Non-GSE Loans

Chart 1

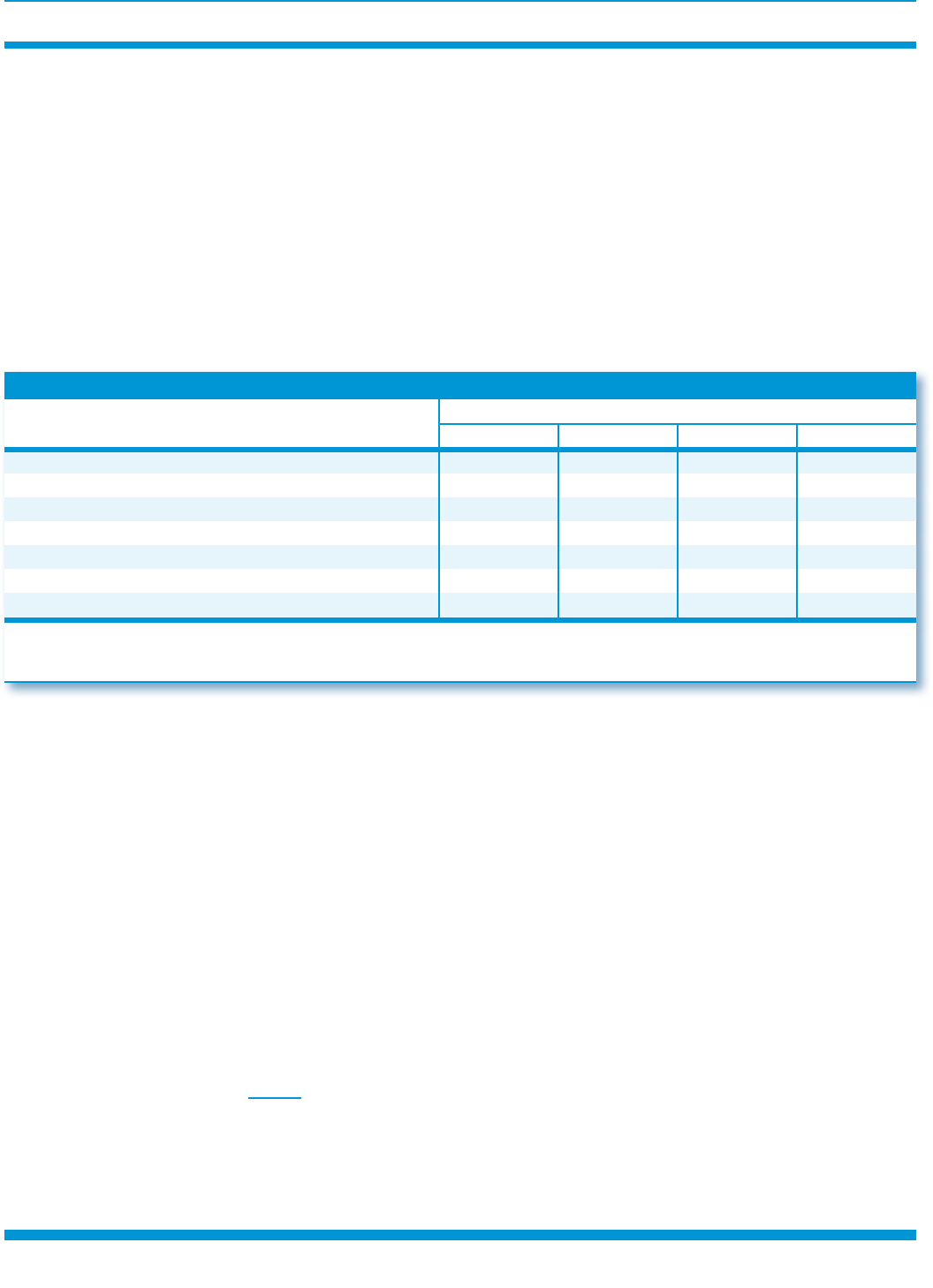

Lending Trends by Sector Nonbank lending also plays an important role over time in other markets. Except for lever-

aged loans, the bank shares of loans outstanding have been generally stable or increas-

ing since 2010. Pre-financial crisis, bank shares of outstanding loans in several categories

declined. In 1–4 family mortgage lending, bank shares decreased from 40percent in 1990

to 25percent in 2010, and in multifamily residential mortgages, from 44percent in 1990 to

29percent in 2010. As shown in the table on the following page, bank shares of commercial

mortgages and agricultural loans grew over this period.

3

For a history of the GSEs, see “A Brief History of the Housing Government-Sponsored Enterprises,” Federal Housing Finance

Agency Office of Inspector General, www.fhfaoig.gov/Content/Files/History%20of%20the%20Government%20Sponsored%20

Enterprises.pdf, and “Our History,” Farm Credit, https://farmcredit.com/history.

FDIC QUAR TERLY

33

BANK AND NONBANK LENDING OVER THE PAST 70 YEARS

Many factors contributed to growth in the nonbank share of loans before the financial

crisis, but the development and growth of loan securitization was an important one. Some

investors prefer to or must hold rated, more-liquid securities like ABS rather than unrated,

less-liquid assets such as loans. In the common securitization model, lenders originate loans

and sell them to nonbanks that package the loans and issue ABS. Loan types with more

standardized terms and more forecastable outcomes—like residential mortgages and some

commercial real estate (CRE) mortgages—are easier to securitize, enabling greater participa-

tion by nonbanks that rely on an originate-to-distribute model. Securitization of other loan

types—like large leveraged loans—involve pools with fewer but larger loans that are rated,

which makes them more easily securitized. On the other hand, commercial and industrial

loans tend to be smaller and more idiosyncratic than the larger leveraged loans, so they are

generally not rated and have not been securitized to the same degree. The following sections

describe the changes in different lending categories.

Bank Share of Loans by Type of Loan

Type of Loans

Bank Share of Loans Outstanding (%)

1990 2000 2010 2018

1–4 family mortgages 40 30 25 24

Leveraged loans NA 25 8 3

CRE mortgages 50 49 47 50

Commercial mortgages 52 54 54 58

Multifamily residential mortgages 44 34 29 33

Consumer credit 52 35 45 42

Agriculture loans 35 46 39 42

Sources: Federal Reserve Flow of Funds (Haver Analytics), S&P Leveraged Commentary and Data, and USDA Economic Research Service.

Notes: Leveraged loans exclude revolving credit-only loans and left and right agent commitments (including administrative, syndication and

documentation agent, and arranger). Data are as of the fourth quarter.

I. 1–4 Family Mortgages

One-to-four family mortgages, including home equity loans and home equity lines of credit,

are loans that are secured by residential units. The share of 1–4 family mortgages outstand-

ing held by banks declined dramatically from 74percent in 1978 to 24percent in second

quarter 2019 as securitization of mortgages became an increasingly larger part of the market.

From 1980 to 2000, the majority of MBS were issued by the GSEs, but private-label MBS

(PLMBS) grew rapidly before the financial crisis.

4

Demand for PLMBS dried up during the

financial crisis and remains well below pre-financial crisis levels, despite recent growth.

5

Government-backed MBS issuance, including GSE issuance, has continued to grow. In

second quarter 2019, GSEs held 63percent of residential mortgages outstanding.

Because of the demand for GSE MBS, both banks and nonbanks sell mortgages to the GSEs.

Since the financial crisis, nonbanks have predominantly offered mortgages that conform to

the criteria established by the GSEs, as nonbanks rely on an originate-to-distribute business

model.

6

Banks are more likely to make jumbo and nonconforming loans that cannot be sold

to the GSEs, and tend to hold more of their residential mortgages. As these banks retain the

risk of the loans, they may perform more thorough underwriting than nonbank lenders who

quickly sell their loans.

4

PLMBS are MBS issued by private financial institutions. They are also called non-agency MBS.

5

PLMBS issuance fell from $1.3 trillion in 2006 to $28 billion in 2012. As of second quarter 2019, private pools held $454 billion in

residential mortgages, about 4 percent of the outstanding residential mortgages.

6

These mortgages are known as conforming loans, since they conform to standards set by the GSEs and are eligible to be

purchased by the GSEs.

2019 • Volume 1 3 • Number 4

34 FDIC QUA RTER LY

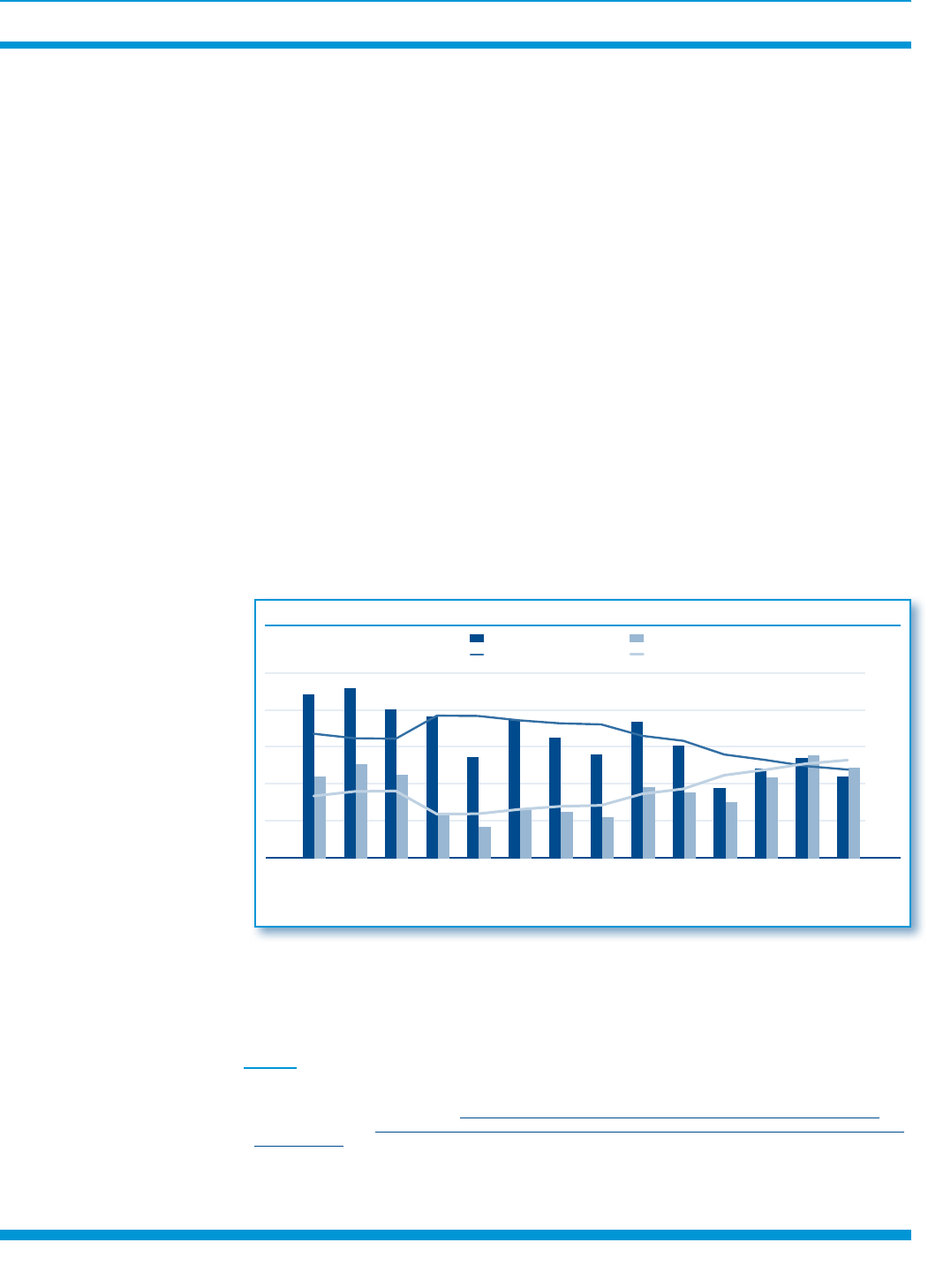

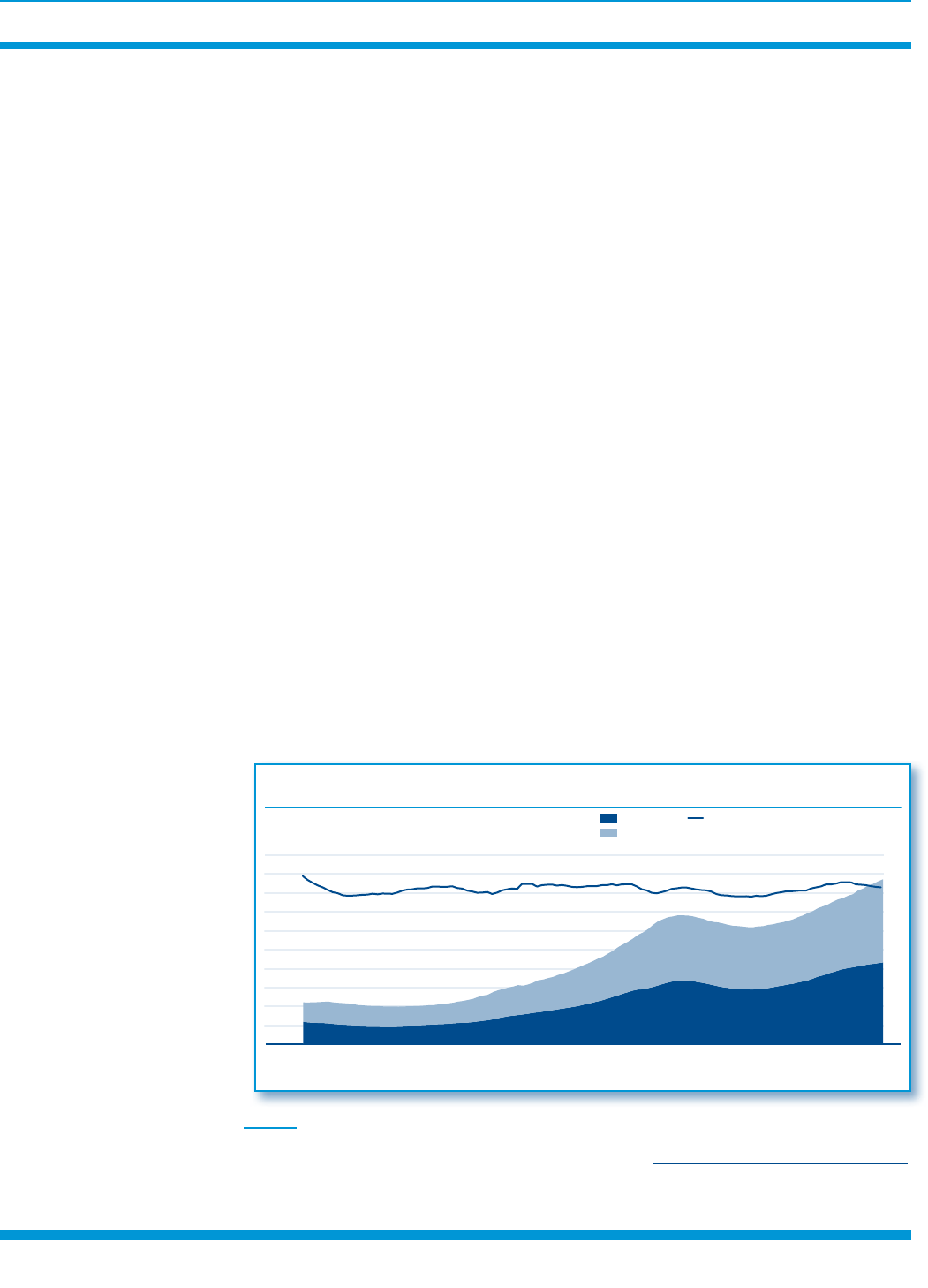

In the early 2000s, bank and nonbank mortgage lenders loosened underwriting standards,

and residential mortgage originations grew rapidly, partly driven by the demand for MBS.

In the financial crisis that began in 2007, PLMBS issuance fell and many nonbank mortgage

lenders failed or merged. The nonbank share of mortgage originations among Home Mort-

gage Disclosure Act (HMDA) report filers fell from 36percent in 2006 to 24percent in 2008

(Chart 2). After the financial crisis, new nonbank lenders entered the market, increasing

from 820 lenders in 2011 to 919 in 2017. The number of bank mortgage lenders fell during

that period. In 2017, nonbanks accounted for 53percent of mortgages originated by HMDA

filers.

7

Nonbanks originate a significant volume of loans for sale to GSEs. GSEs have loos-

ened underwriting criteria in recent years, which could increase financial system vulner-

ability if pronounced housing market stress occurs (see accompanying article, “Trends in

Mortgage Origination and Servicing: Nonbanks in the Post-Crisis Period”).

Mortgage servicing also has shifted from banks to nonbanks. Nonbanks held 42percent of

mortgage servicing rights held by the top 25 servicers in 2018, up from 4percent in 2008

and 38percent in 2000. Large bank sales of financial crisis-era legacy servicing portfolios

contributed to the shift in servicing from banks to nonbanks. Fines, legal fees, and other

heightened expenses associated with litigation and with nonperforming loans in financial

crisis-era servicing portfolios negatively affected profitability at some banks and may have

deterred growth in servicing portfolios after the financial crisis.

8

Changes in the regula-

tory capital treatment of mortgage servicing assets may have contributed to the reduction in

mortgage servicing rights by large banks.

9

Overall servicing volume rebounded to $10.9tril-

lion in 2018, only slightly below the peak of $11.2trillion in 2007 and more than double the

$5.1trillion reported in2000.

10

Nonbanks Increased Mortgage Originations Aer the Financial Crisis

Source: FDIC analysis of Home Mortgage Disclosure Act data.

Notes: Nonbanks include all Department of Housing and Urban Development reporters. Banks include banks, credit unions, and their aliates.

Data are limited to single-family residential mortgage originations, dened as rst-lien purchase or renance loans secured by an owner-occupied,

1–4 family unit, site-built property.

Market Share

Percent

Origination Volume

$ Billions

47.5

52.5

0

20

40

60

80

100

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0

200

400

600

800

1,000

1,200

1,400

1,600

Bank Volume (Right Axis) Nonbank Volume (Right Axis)

Bank Share (Le Axis) Nonbank Share (Le Axis)

Chart 2

7

FDIC analysis of HMDA data. Bank mortgage lenders are banks that file HMDA reports.

8

FDIC, Board of Governors of the Federal Reserve System (FRB), Office of the Comptroller of the Currency (OCC), National

Credit Union Administration (NCUA), “Report to the Congress on the Effect of Capital Rules on Mortgage Servicing Assets,”

June 2016, pages 23–25, https://www.federalreserve.gov/publications/other-reports/files/effect-capital-rules-mortgage-servicing-

assets-201606.pdf.

9

FDIC, FRB, OCC, NCUA: 29–31.

10

FDIC analysis of Inside Mortgage Finance data.

FDIC QUAR TERLY

35

BANK AND NONBANK LENDING OVER THE PAST 70 YEARS

II. Corporate Debt and Leveraged Lending

Loans to corporations, including leveraged loans, have shifted out of banks over the past

60years, and corporations have increased their use of debt securities to fund their busi-

nesses. Leveraged loans are syndicated loans made to below-investment-grade corporate

borrowers.

11

Corporate debt securities include corporate bonds and commercial paper.

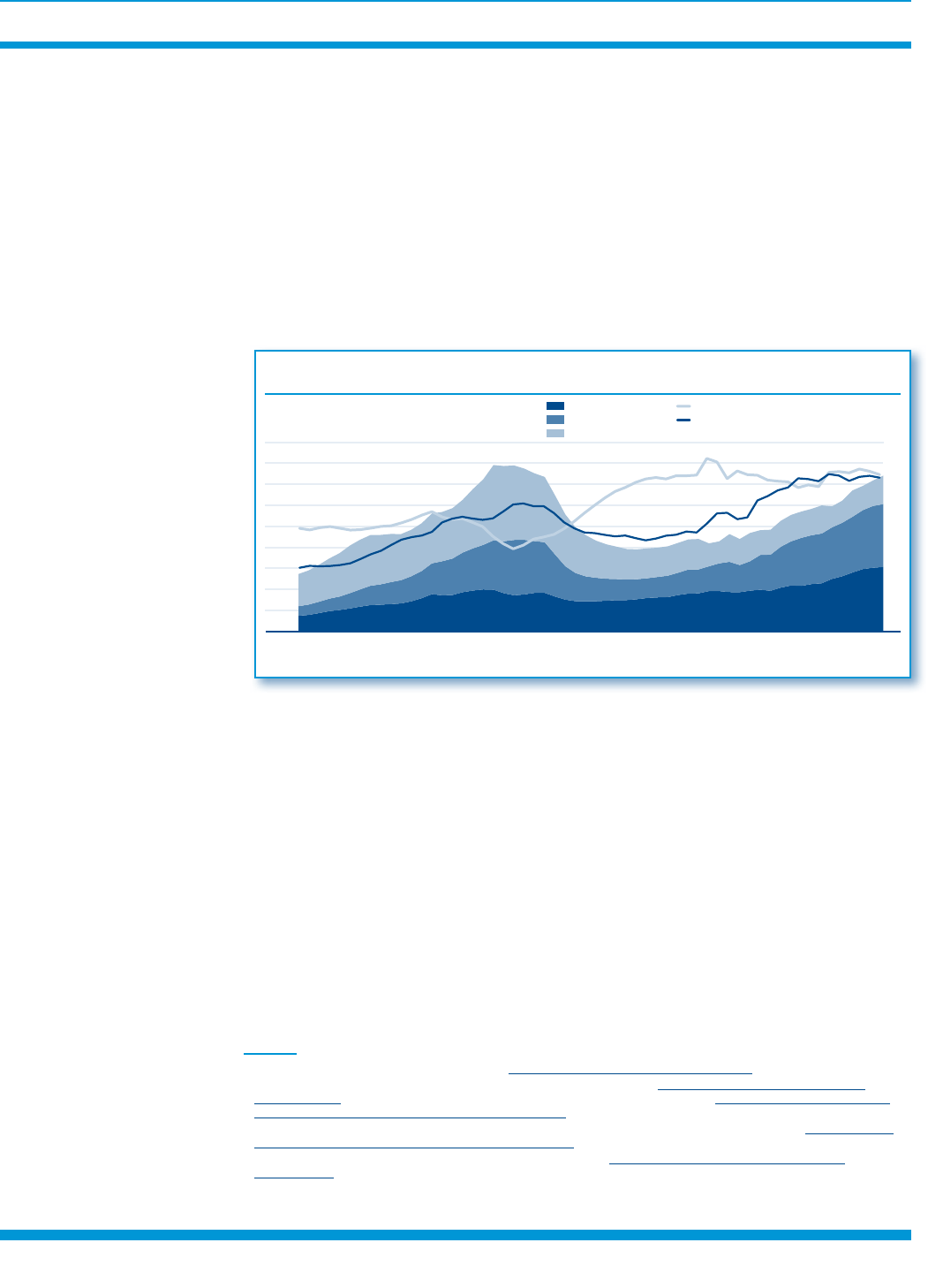

Institutional syndicated leveraged loans outstanding increased from $100billion in 2000

to $1trillion in 2018. Originations fell to $77billion in 2009 but recovered to $625billion

in 2018. The share of primary leveraged loan purchases made by banks declined from

30percent in 1994 to 3percent in 2018 (Chart 3). Banks arrange almost all of the loans by

providing information about the loan to investors and putting together a group of buyers.

Banks often administer the loans. Of the top 20 leveraged loan administrative agents in the

Leveraged Commentary and Data database for 2018, 18 were commercial banks or invest-

ment banks.

Over the past ten years, nonfinancial corporate debt securities grew from $4trillion in first

quarter 2009 to $6trillion in first quarter 2019. Nonbank investors hold the majority of

outstanding financial and nonfinancial corporate bonds. As of second quarter 2019, banks

held only 3percent of outstanding corporate bonds. Banks also underwrite corporate debt

securities and provide other investment banking services.

Corporate debt has grown since 2008. Investors increased their demand for high-yielding

leveraged loans and corporate debt securities, as they were willing to accept greater risk. To

help satisfy the demand, underwriting standards deteriorated in this market and lenders

issued loans to riskier corporations. The share of leveraged loans that lack strong covenants

grew from near zeropercent in the early 2000s, to 29percent in 2007, and to 85percent in

2018.

12

The leverage of the borrowers also increased over the same period.

13

Therefore,

U.S. Bank Share of Primary Leveraged Loan Purchases Has Declined Signicantly,

ough Risk Exposure Remains

Source: S&P LCD.

Notes: Excludes revolving credit-only loans as well as le and right agent commitments (including administrative, syndication and documentation agent,

and arranger). Data are through second quarter 2019.

Share of Primary Leveraged Loan Purchases

Percent

0

10

20

30

40

50

60

70

80

90

100

1994 1997 2000 2003 2006 2009 2012 2015 2018

CLOs, Insurance Companies,

and Loan, Hedge, and High-Yield Funds

Finance Companies and Securities Firms

Foreign Banks

U.S. Banks

Chart 3

11

Unless otherwise noted, we follow the S&P Global Market Intelligence Leveraged Commentary and Data definition of leveraged

loans, which includes all syndicated loans that are below investment grade, are senior secured, and have a minimum spread of 125

basis points over LIBOR.

12

Leveraged loans with strong covenants have both “incurrence covenants,” which require financial tests if the borrower wants

to perform certain actions such as paying dividends, and “maintenance covenants,” which require the borrower to regularly pass

financial health tests such as maximum leverage levels and minimum interest coverage, or risk defaulting on the loan. Covenant-

lite leveraged loans have incurrence covenants but lack maintenance covenants.

13

Leverage is measured as the ratio of total debt to earnings before interest, tax, depreciation, and amortization (EBITDA). The

average debt-to-EBITDA ratio for leveraged loan borrowers was 5.2 at year-end 2018, its highest level since at least 2002 and well

above the 4.9 level that it reached in 2007.

2019 • Volume 1 3 • Number 4

36 FDIC QUA RTER LY

future recoveries on defaulted leveraged loans are likely to be lower than previously expe-

rienced because of lower credit quality and weakened lender protections. Risks have been

building in corporate debt securities as well. Most of the change in corporate debt outstand-

ing over the past ten years was from lower-rated investment grade bonds and the highest-

rated high-yield bonds, rather than from higher-rated investment grade bonds.

14

Banks’ direct exposure to institutional leveraged loans has fallen during the past 20 years.

But some banks still have direct exposure to revolving credit facilities that are often part of

a leveraged loan deal and additional indirect exposure to institutional leveraged loans. This

exposure includes (1) pro rata leveraged loans, (2) warehouse lines of credit used for collat-

eralized loan obligations, and (3)subscription finance loans. Bank exposure to risk from

nonbanks that participate in leveraged lending is opaque, and the nature and size of the risk

is obscured. Risk is difficult to quantify because it is not reported in a standardized manner.

III. Other Lending Sectors

The migration of risks and activities between banks and nonbanks in lending sectors other

than 1–4 family mortgages and leveraged lending has been less pronounced. This section

summarizes market share developments in commercial real estate lending, agriculture lend-

ing, and consumer credit. Bank shares of outstanding loans in these sectors are significantly

higher than in 1–4 family mortgage lending and in leveraged loans. Moreover, bank shares of

outstanding commercial real estate loans and agriculture loans have increased, rather than

decreased, since 2010.

15

CRE Loans. CRE loans include loans secured by commercial or multifamily residential

properties and unsecured loans to finance CRE activities. Banks have regained market share

of CRE mortgages after a decline during the financial crisis (Chart 4). The bank share of

commercial mortgages has been relatively steady at around 50 to 55percent since the mid-

1970s. In second quarter 2019, banks held 59percent of commercial mortgages. In contrast,

the bank share of multifamily residential mortgages decreased substantially between 1990

and 2012 and has modestly recovered since. Changes in bank share are largely attributable to

GSE securitization activity. In second quarter 2019, GSEs held about half of the outstanding

multifamily residential mortgages and banks held 33percent.

e Bank Share of Commercial Real Estate Mortgages Has Been Around 50 Percent

Since the 1990s

Source: Federal Reserve Flow of Funds (Haver Analytics).

Note: Dollar values are adjusted for ination.

Loans Outstanding

$ Billion 2012

Bank Bank Share

Nonbank

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Bank Share of Loans

Percent

1992 1995 1998 2001 2004 2007 2010 2013 2016 2019

0

10

20

30

40

50

60

Chart 4

14

ICE data services.

15

For discussion of risks in these lending sectors see “FDIC 2019 Risk Review,” https://www.fdic.gov/bank/analytical/risk-review/

index.html.

FDIC QUAR TERLY

37

BANK AND NONBANK LENDING OVER THE PAST 70 YEARS

Agriculture Lending. Quarterly Reports of Condition and Income (Call Reports) filed by

FDIC-insured banks classify agricultural loans as (1) loans secured by agricultural land and

(2) operating loans to farms and agricultural businesses. Agriculture loans are made primar-

ily through banks and the Farm Credit System, a government-sponsored system of borrower-

owned lenders that provide loans and related services to many rural customers. The bank

share of agriculture lending is 42percent and has varied between 37 and 45percent since

the early 1990s (Chart5). The share of loans held by the Farm Credit System grew through

the 1990s and early 2000s and is now around 41percent of outstanding agriculture loans. In

2018, commercial banks and the Farm Credit System held 83percent of farm sector loans,

and the Farm Service Agency, Farmer Mac, life insurance companies, and individuals held

the remainder of loans outstanding.

16

e Bank Share of Agricultural Loans Has Been Around 40 Percent Since the Mid-1990s,

While the Farm Credit System Share Has Risen

Source: USDA Economics Research Service.

Note: Dollar values are adjusted for ination.

Farm Debt Outstanding

$ Billions 2012

Commercial BanksBank Share

Farm Credit System

Other

Share of Debt

Percent

0

50

100

150

200

250

300

350

400

450

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Farm Credit System Share

0

5

10

15

20

25

30

35

40

45

50

Chart 5

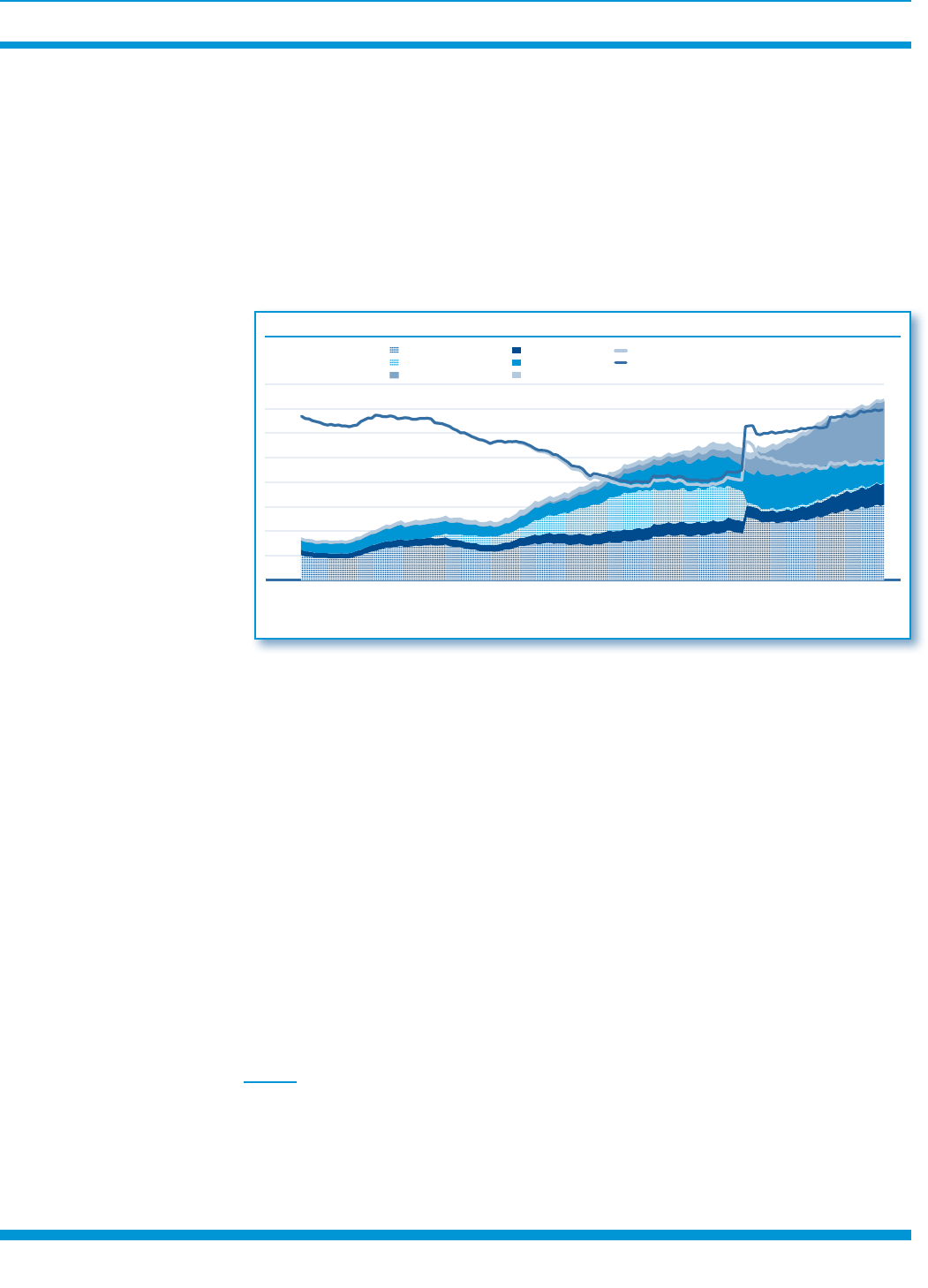

Consumer Credit. The bank share of consumer credit—loans to consumers that are not

backed by real estate—fell from the late 1980s to the early 2000s because of securitization.

Starting in the late 1980s, ABS backed by credit card debt, auto loans, and private student

loans became widely used.

17

The bank share of consumer credit fell from 52percent in fourth

quarter 1990 to 35percent in fourth quarter 2000. An accounting change in first quarter

2010, however, moved most ABS back onto the balance sheets of the firms that controlled

the securities, causing a jump in the reported share of consumer credit held by banks from

35percent in fourth quarter 2009 to 49percent in first quarter 2010.

18

Because many of these

loans are still securitized, some of the credit risk passes to the purchasers of the ABS even

if the loans are on the bank’s balance sheet. And in 2010, the federal government stopped

subsidizing private lenders to make student loans and instead originates all federally subsi-

dized loans itself.

19

This shift caused another decline in the bank share of consumer credit

because only the federal government can make federally subsidized student loans (Chart 6).

If student loans continue to grow faster than other forms of consumer credit, the bank share

of consumer credit may continue to decline.

16

USDA/ERS Farm Income and Wealth Statistics, https://data.ers.usda.gov/reports.aspx?ID=17835.

17

Sumit Agarwal, Jacqueline Barett, Crystal Cun, and Mariacristina De Nardi, “The Asset-Backed Securities Market, the

Crisis, and TALF,” Federal Reserve Bank of Chicago Economic Perspectives 34, no. 4 (2010), www.chicagofed.org/publications/

economic-perspectives/2010/4q-agarwal-barrett-cun-denardi.

18

The accounting change was released in Financial Accounting Standards Board Statements 166 and 167. See https://www.fasb.

org/jsp/FASB/FASBContent_C/NewsPage&cid=1176156240834 for a detailed explanation.

19

H.R. 4872: “Health Care and Education Reconciliation Act of 2010,” https://www.congress.gov/bill/111th-congress/

house-bill/4872.

2019 • Volume 1 3 • Number 4

38 FDIC QUA RTER LY

While the shift of consumer credit from banks to nonbank financial companies has been

less pronounced than in other bank lending categories, consumer lending within the bank-

ing industry has become more concentrated. The top ten credit card lending banks held

34percent of bank credit card loans in 1984 and 88percent of bank credit card loans in

second quarter 2019. The top two banks alone hold more than 30percent of credit card

loans.

20

In auto lending, the bank share of outstanding auto loans changed little from first

quarter 2011 (35percent) to first quarter 2018 (33percent).

21

But the top ten large bank auto

lenders hold 71percent of outstanding bank auto loans, according to second quarter 2019

Call Reports.

e Growth of ABS and Federal Student Loans Lowered the Bank Share of Consumer Credit

Source: Federal Reserve Flow of Funds (Haver Analytics).

Notes: Dollar values are adjusted for ination. Financial Accounting Standards Board Statements No. 166 and No. 167 resulted in the consolidation

of a large amount of securitized loan balances back onto lenders’ balance sheets in rst quarter 2010.

Loans Outstanding

$ Billion 2012

Banks Credit Unions

Issuers of ABS Other Financial

Federal Government

Other Nonnancial

Bank Share of Loans

Percen

t

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1980 1985 1990 1995 2000 2005 2010 2015 2019

Bank Share

Bank Share Excluding Fed. Student Loans

0

10

20

30

40

50

60

70

Chart 6

IV. Lending to Nondepository Financial Institutions

Although direct bank exposure to some lending categories has fallen, banks may still have

indirect exposure through lending to nonbank financial institutions (NBFI). Bank lending to

NBFIs grew from about $50billion in 2010 to $442billion in second quarter 2019 (Chart7).

NBFI loans include loans to special purpose vehicles, private equity funds, real estate invest-

ment trusts (REIT), and nonbank mortgage lenders. About 11percent of banks held NBFI

loans in second quarter 2019, and the four largest banks—JPMorgan Chase N.A., Bank of

America N.A., Citibank N.A., and Wells Fargo N.A.—held about half of the total of NBFI

loans outstanding.

22

Bank supervisory experience suggests that outside of the large banks,

most NBFI lending is to nonbank mortgage lenders or to MBS warehouse lines.

23

Through

these loans, banks retain exposure to many of the loans that have shifted to nonbanks.

Other potential exposure includes loans to business development companies, other business

lenders, private equity funds, venture capital funds, real estate funds, and REITs. These loans

may be accounted for under different loan categories on a bank balance sheet, which can

make it difficult to identify a bank’s credit risk exposure to NBFIs.

20

Credit card data are based on Call Reports. Citibank held 17 percent of bank credit card loans, and JPMorgan Chase N.A. held

16 percent of credit card loans.

21

Experian Automotive. In first quarter 2011, auto loans became a separate category on Call Reports. Before then, auto loans were

included with other consumer loans and concentrations could not be identified.

22

FDIC analysis of Call Reports.

23

FDIC.

FDIC QUAR TERLY

39

BANK AND NONBANK LENDING OVER THE PAST 70 YEARS

Banks may also hold securities that expose them to risks from nonbanks. For example, banks

may hold collateralized loan obligations that include leveraged loans. Because Call Reports

do not require detail about these asset classes, understanding the underlying credit risk of a

bank’s portfolios of securities and loans to nonbank financial institutions is difficult.

Loans to Nonbank Financial Institutions Have Grown Dramatically Since Data Collection Began

Source: FDIC.

Note: Quarterly data through second quarter 2019. NBFI stands for nonbank nancial institution.

Loans to Nonbank Financial Institutions

$ Billions

Share of Banks With Loans to NBFIs

Percent

0

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

0

2

4

6

8

10

12

Community Bank Loans to NBFIs (Le Axis)

Noncommunity Bank Loans to NBFIs (Le Axis)

Percent of Banks With Loans to NBFIs (Right Axis)

Chart 7

Conclusion The banking industry and its activities have changed dramatically in 70 years. Securitization

is a primary cause of the shift in loan origination from banks to nonbanks. If less-regulated

financial institutions play a larger role in lending, the shift may alter underwriting stan-

dards when loan demand increases. For private securities such as PLMBS, this shift creates

a market that is more liquid but could dry up quickly in a financial crisis, as we saw in the

Great Recession. Studying where loans have shifted in lending sectors and the linkages

among lenders deepens our understanding of risk in the financial system. The FDIC will

publish a series of articles that look closely at the factors driving these trends and the related

risks of residential mortgages and corporate debt and leveraged lending.

Author:

Kathryn Fritzdixon

Senior Financial Economist

Division of Insurance and Research